Crude to Chemicals Refineries Led the Chinese Players to Hegemony in the Global Petrochemical Market

Introduction and Context

The crude oil refining industry currently faces significant challenges: raw material price volatility, growing societal pressure to reduce environmental impacts, and increasingly compressed refining margins. A more recent threat is the contraction of the consumer market for transportation fuels. In recent years, news of countries intending to reduce or ban the

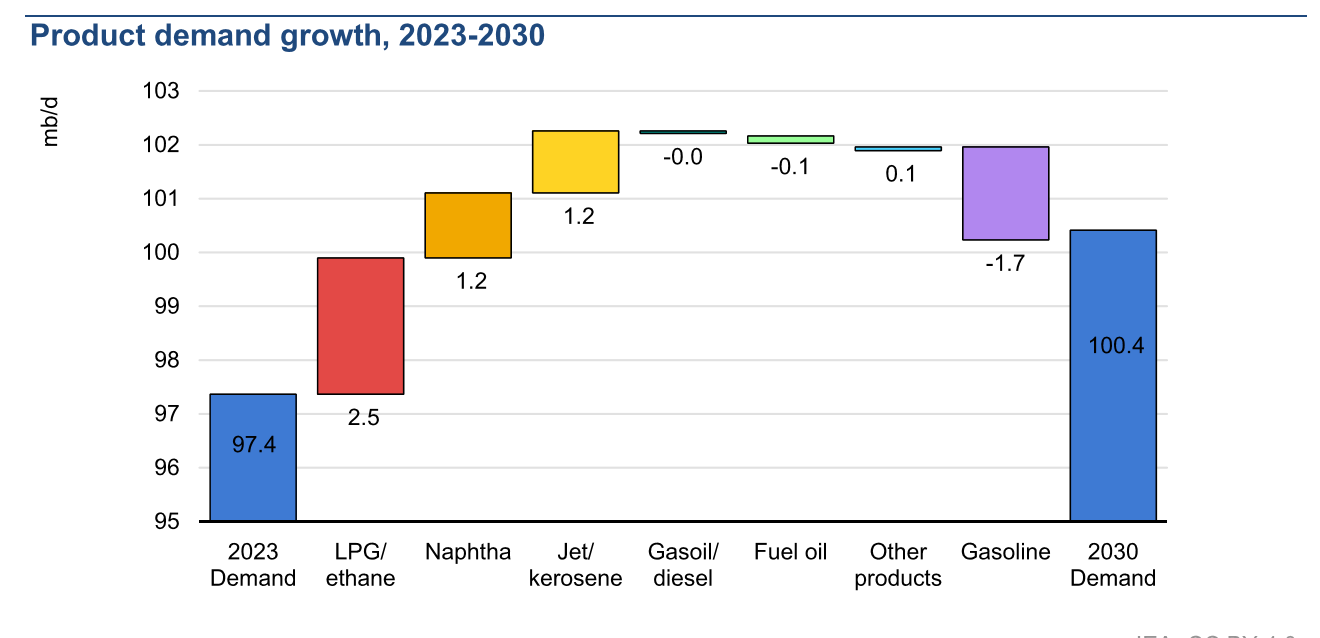

production of fossil-fuel-powered vehicles — particularly across the European market — has become commonplace. Despite these forecasts, transportation fuels remain the downstream industry's primary revenue driver. However, as shown in Figure 1, a clear and significant downward trend in transportation fuel consumption is underway, with gasoline demand declining most noticeably.

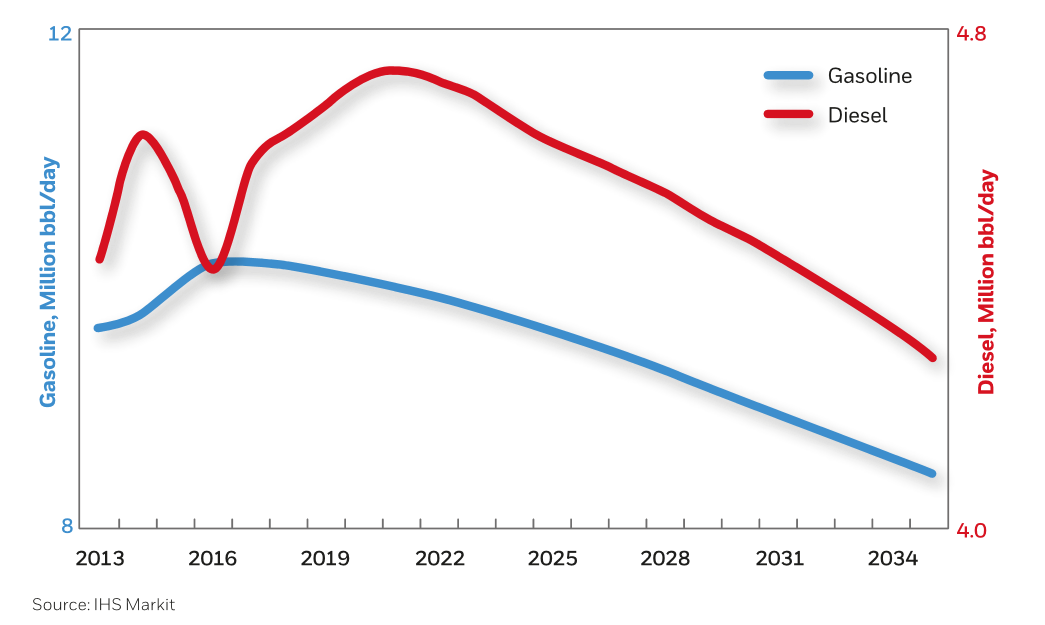

Figure 1 – Global Oil Demand by Derivative (International Energy Agency, 2024)

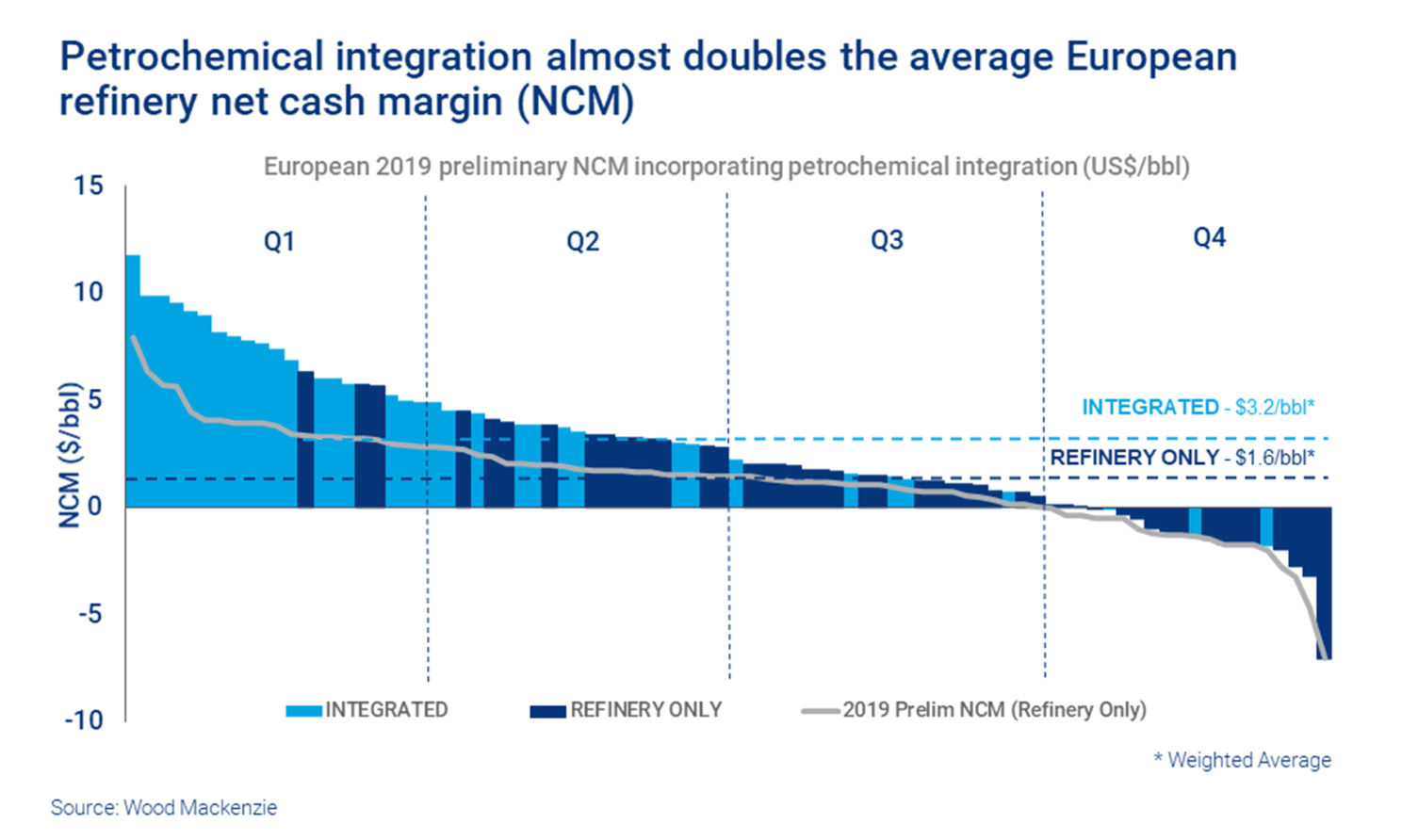

According to Figure 1, petrochemical demand is on a rising trajectory while transportation fuels trend downward — gasoline demand specifically is projected to fall by approximately 1.7%. Wood Mackenzie data (Figure 2) further highlights that, due to their higher value-addedoutput, more integrated refiners consistently achieve higher net cash margins than conventional refiners whose operations remain focused on transportation fuels.

Figure 2 – Refining Margins to Integrated and Non-Integrated Refining Hardware (Wood Mackenzie, 2020)

NCM = Net Cash Margins

Improving fuel efficiency and the growing market penetration of electric vehicles are directly associated with the declining share of transportation fuels in global crude oil demand. Emerging technologies such as additive manufacturing (3D printing) also carry significant potential to further reduce transportation demand — and with it, transportation fuel consumption. Additionally, the greater availability of lighter crude oil types favors an oversupply of lighter derivatives, facilitating petrochemical production over transportation fuels while reinforcing the higher added value of petrochemical outputs relative to fuels. As shown in Figure 3, demand for petrochemicals is projected to grow in the coming years, representing an attractive opportunity for refiners seeking to maintain a leading role in the market.

Figure 3 – Growing Trend in the Demand for Petrochemical Intermediates (IEA, 2025)

According to Figure 3, significant growth in the market for petrochemical intermediates is expected. Refining configurations capable of maximizing the yield of these derivatives can offer a substantial competitive advantage through closer integration with petrochemical assets and higher value addition to processed crude oil. Taking the North American market as an example, a sustained decline in transportation fuel demand is anticipated, as illustrated in Figure 4.

Figure 4 – Transportation Fuels Demand in the North American Market (UOP Company, 2021)

Another major structural shift reinforcing the need for high-conversion refining configurations is the IMO 2020 regulation. This regulatory change further increased pressure on refiners with limited bottom-barrel conversion capacity, requiring greater ability to add value to residual streams — in particular, sulfur content was reduced from 3.5% (by mass) to 0.5%. Refiners with ready access to low-sulfur crudes hold a relative competitive advantage in this environment: they can rely on relatively low-cost residue upgrading technologies — such as Solvent Deasphalting and Delayed Coking — to produce the new compliant marine fuel oil (bunker fuel). However, these players represent a minority. The majority of refiners must either source low-sulfur crudes at a premium, further compressing their margins, or invest in deep bottom-barrel conversion technologies to preserve competitiveness. For these operators, deep residue upgrading via hydrocracking technologies can offer significant operational flexibility, despite requiring substantial capital expenditure. In this context — characterized by the need for higher bottom-barrel value addition and a growing petrochemical market — refiners with adequate bottom-barrel conversion capacity are best positioned to achieve durable competitive advantage in the downstream sector.

Applying Blue Ocean Strategy to the Downstream Industry

The dynamics described above align well with the framework proposed by W. Chan Kim and Renée Mauborgne in their Harvard Business Review article, "Blue Ocean Strategy." The authors define a red ocean as a conventional market where players compete for existing demand, focus on defeating competitors, and generate limited differentiation and low profitability. A blue ocean, by contrast, is characterized by the pursuit of underexplored or unexplored market space, the creation of new demand, and meaningful differentiation. This framework can be applied — with certain commodity-market-specific caveats — to the downstream industry, mapping the traditional transportation fuels refinery against the petrochemical sector.

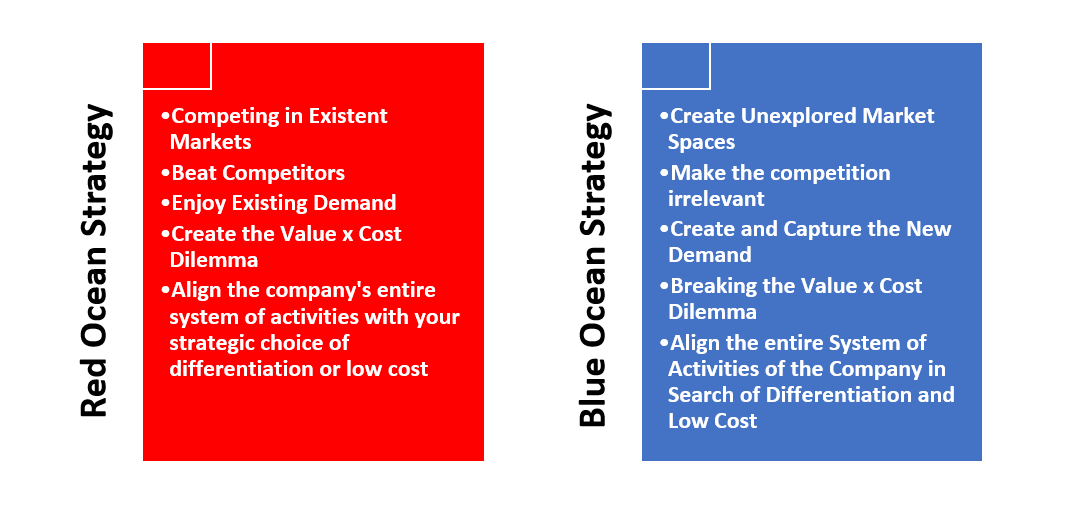

The transportation fuels market embodies the characteristics of a red ocean: margins are low, competition is intense, and differentiation capacity is minimal. The petrochemicals sector, by contrast, functions as a blue ocean — accessible to relatively few players operating under competitive conditions, commanding higher refining margins, and enabling clear differentiation from fuel-focused refiners. Figure 5 illustrates the fundamental conceptual difference between the Blue and Red Ocean strategies.

Figure 5 – Differences between Blue and Red Ocean Strategies (KIM & MAUBORGNE, 2004)

Market forecasts confirm that refiners capable of shifting output toward petrochemicals stand to achieve strong economic performance in the near term. In this context, crude oil to chemicals (COTC) technologies can offer even greater competitive advantage to refiners with sufficient capital investment capacity.

It may seem difficult to apply the concept of "differentiation" to the downstream industry, given that it fundamentally deals in commodities. However, differentiation here refers specifically to the ability to extract greater added value from processed crude oil — and as outlined above, this today translates directly into the capacity to maximize petrochemical yields, creating a meaningful divide between integrated and non-integrated players.

Petrochemical Market Outlook

Using 2024 as the baseline, the global petrochemical market reached a total value of USD 659.22 billion, with a projected compound annual growth rate (CAGR) of 6.11% between 2024 and 2033, as presented in Figure 6.

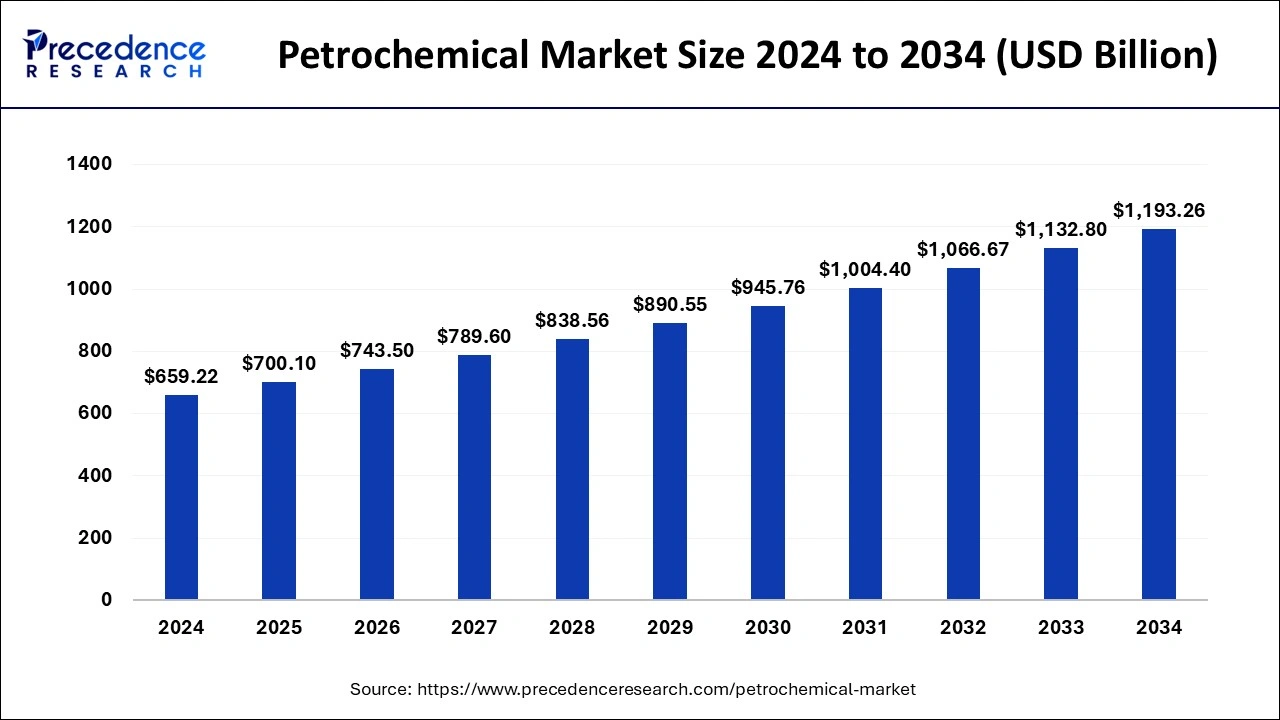

Figure 6 – Petrochemical Market Size Forecast 2024-2034 (Precedence Research, 2025)

Based on this trajectory, the petrochemical market could approach USD 1,193.26 billion by 2034, reinforcing the long-term attractiveness of the petrochemical sector for refiners operating in a contracting transportation fuels environment under growing pressure to reduce the carbon intensity of the energy matrix.

Considering just the aromatics solvents market (Benzene, Toluene, and Xylenes — BTX), the expected CAGR between 2021 and 2030 is 4.8%, leading the aromatics solvent market to reach USD 8.1 billion by 2030, again according to Precedence Research data.

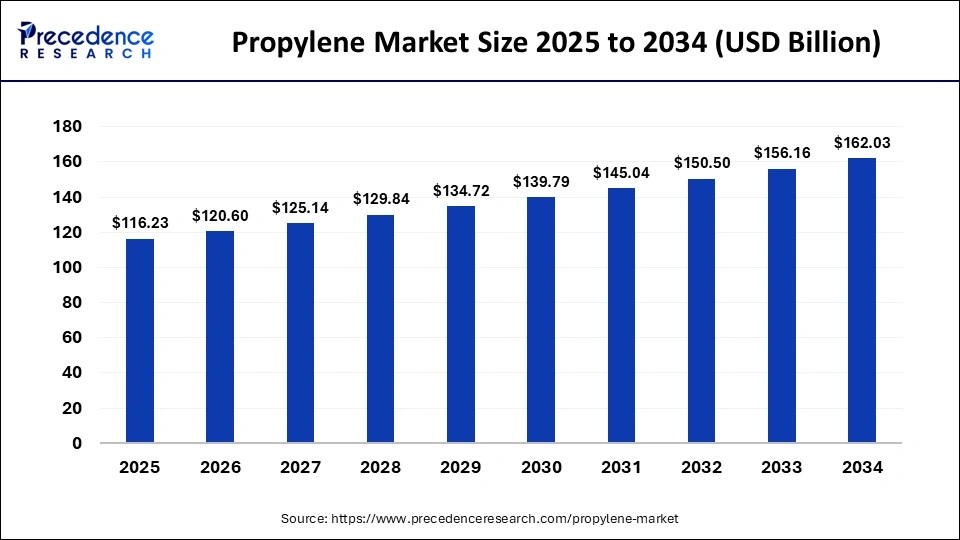

The propylene market presents an even more encouraging outlook for investments in dedicated on-purpose propylene production routes. Figure 7 presents the propylene market size projections for the coming years.

Figure 7 – Evolution of Propylene Market Size for the next years (Precedence Research, 2024)

According to Figure 7, the propylene market could exceed USD 160 billion by 2034, growing at an annual rate of 3.76%, with Asia representing the largest regional market, as expected.

Synergies between Refining and Petrochemical Assets – Petrochemical Integration

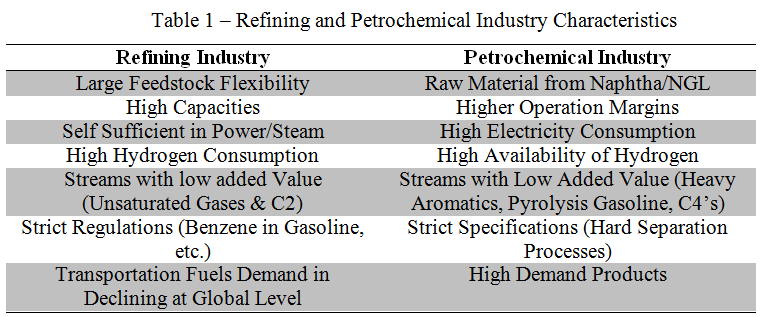

The strategic rationale for closer integration between the refining and petrochemical industries is to identify and capture the existing synergy opportunities between both downstream sectors, generating value across the entire crude oil production chain. Table 1 presents the main characteristics of each industry and their synergy potential.

As previously noted, the petrochemical industry has grown at considerably higher rates than the transportation fuels market in recent years. It also represents a more noble and less environmentally aggressive end use for crude oil derivatives. The technological bases of both industries are similar, creating synergy opportunities capable of reducing operational costs and adding value to refinery-produced derivatives.

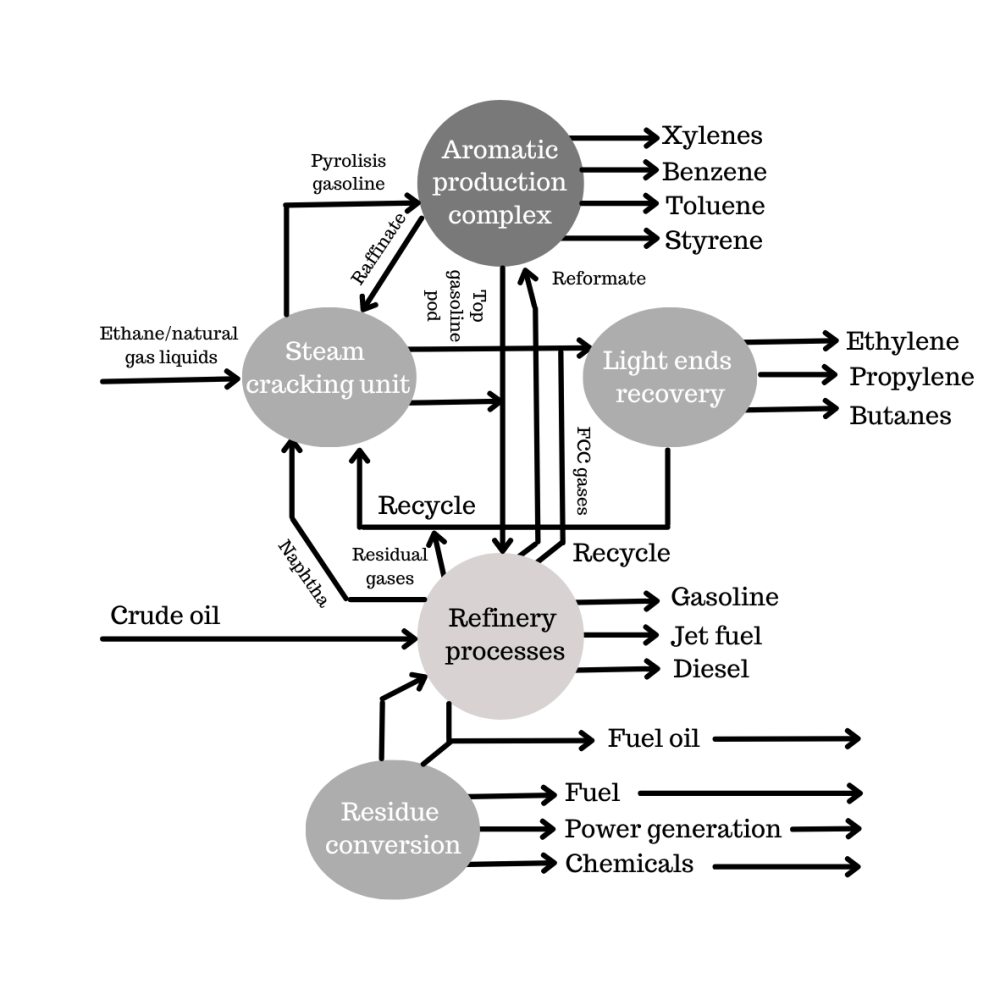

Figure 8 presents a block diagram illustrating selected integration possibilities between refining processes and the petrochemical industry.

Figure 8 – Synergies between Refining and Petrochemical Processes

Process streams considered low in added value to refiners — such as fuel gas (C2) — are attractive raw materials for the petrochemical industry. Conversely, streams considered residual in petrochemical operations — butanes, pyrolysis gasoline, and heavy aromatics — can be reintegrated into refinery fuel pools to help meet environmental and quality specifications for transportation fuels. The degree of achievable integration depends on the refining scheme adopted by the refinery and the characteristics of its consumer market. Units such as Fluid Catalytic Cracking (FCC) and Catalytic Reforming can be optimized to maximize petrochemical intermediate production at the expense of contributions to the fuels pool. In the case of FCC, purpose-built petrochemical FCC units aim to reduce fuel-pool stream generation to a minimum; however, the capital investment is high, as the severe operating conditions require the use of specialized, premium-grade metallurgical materials.

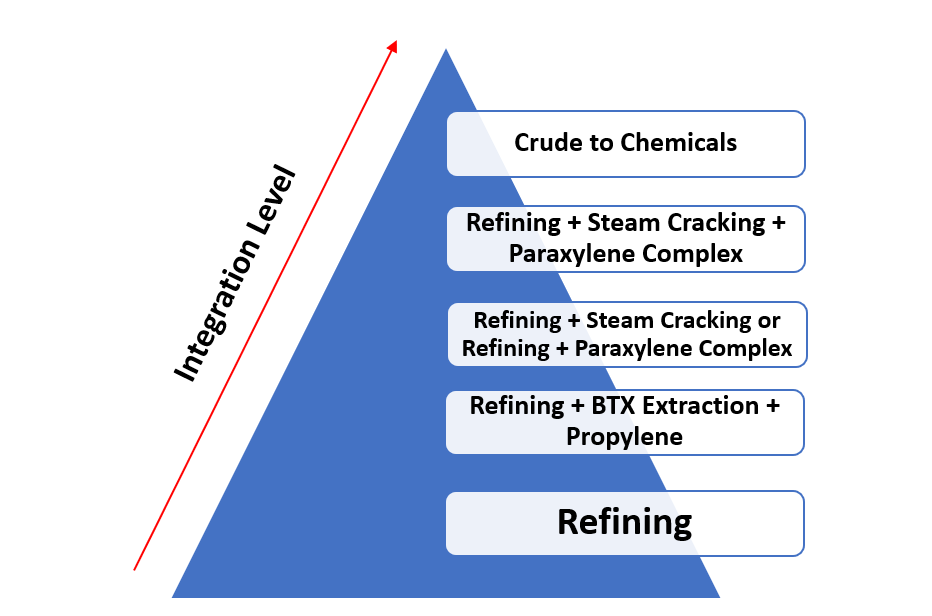

IHS Markit has proposed a classification of petrochemical integration levels, as presented in Figure 9.

Figure 9 – Petrochemical Integration Levels (IHS Markit, 2018)

According to this classification, crude to chemicals (COTC) refineries represent the maximum level of petrochemical integration, where processed crude oil is entirely converted into petrochemical intermediates such as ethylene, propylene, and BTX. Given the current downstream market environment, crude to chemicals refineries offer the differentiation necessary to position players within the Blue Ocean, as described above.

The Crude Oil to Chemicals Refining Assets

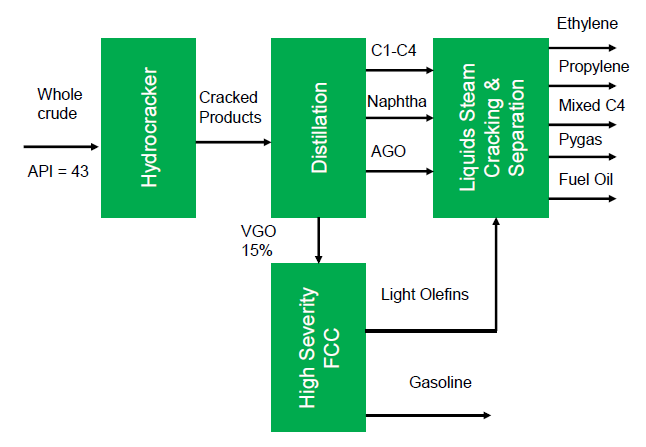

In response to the growing petrochemical market, its higher added value, and the declining demand trend for transportation fuels, a number of refiners and technology developers have dedicated significant efforts to developing crude to chemicals refining assets. One of the most prominent players to invest in this direction is Saudi Aramco, whose concept is based on the direct conversion of crude oil to petrochemical intermediates, as illustrated in Figure 10.

Figure 10 – Saudi Aramco Crude Oil to Chemicals Concept (IHS Markit, 2017)

The process shown in Figure 10 leverages the quality of the feedstock crude and employs deep conversion technologies, including high-severity or petrochemical FCC units and deep hydrocracking. The processed crude oil is light with low residual carbon content — a characteristic common to Middle Eastern crudes. The processing scheme applies deep catalytic conversion to achieve maximum conversion to light olefins, with petrochemical FCC units playing a central role in ensuring high added value from the processed crude.

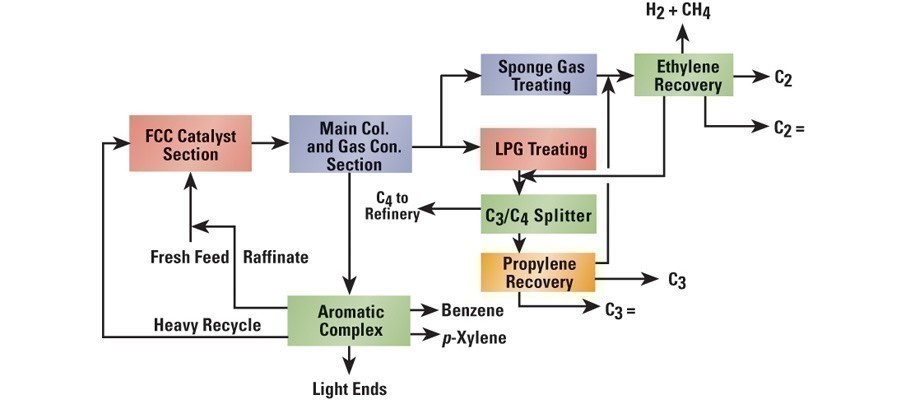

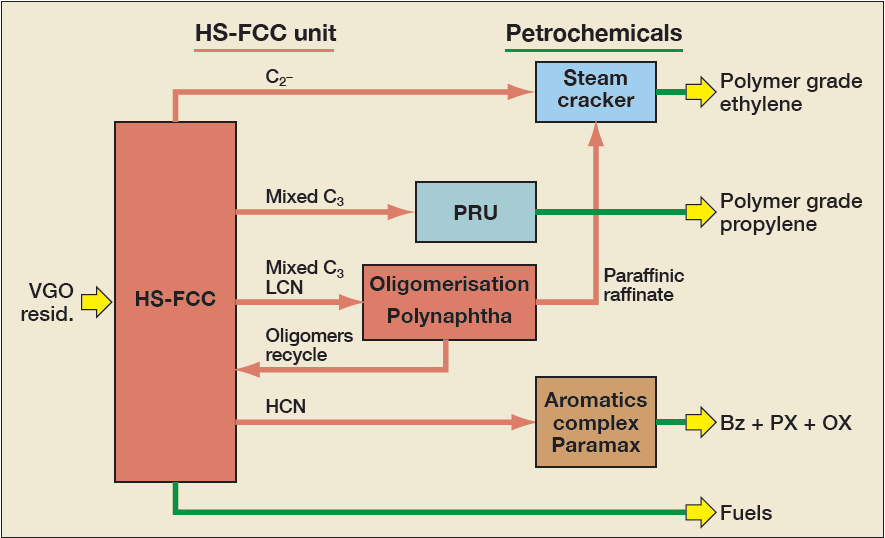

One example of an FCC technology developed specifically to maximize petrochemical intermediate production is the PetroFCC™ process by UOP Company. This process combines a petrochemical FCC unit with an optimized separation section designed to produce raw materials for petrochemical process plants, as presented in Figure 11. Other available technologies include the HS-FCC™ process commercialized by Axens Company and the INDMAX™ process licensed by Lummus Company. The basic process flow diagram for the HS-FCC™ technology is presented in Figure 12.

Figure 11 – PetroFCC™ Process Technology by UOP Company.

It is important to note that both technologies presented in Figures 11 and 12 are based on petrochemical FCC units with special designs to accommodate more severe operating conditions.

Figure 12 – HS-FCC™ Process Technology by Axens Company.

In petrochemical FCC units, reaction temperatures reach 600°C and higher catalyst circulation rates increase gas production, requiring a scaled-up gas separation section. The elevated thermal demand makes it advantageous to operate the catalyst regenerator in total combustion mode, which in turn requires the installation of a catalyst cooler system.

The total combustion mode option must also consider the refinery's overall thermal balance: in this configuration there is no possibility of generating steam in a CO boiler. Furthermore, the higher temperatures in the regenerator demand premium-grade metallurgy, significantly increasing the installation costs of these units — which may be prohibitive for refiners with restricted access to capital.

The installation of petrochemical catalytic cracking units requires a thorough economic study that accounts for both high capital investment and elevated operational costs. However, forecasts indicate growth of approximately 4.0% per year in the market for petrochemical intermediates through 2025, making capital investment aimed at growing market share in the petrochemical sector an attractive proposition — enabling favorable competitive positioning through maximization of petrochemical intermediates.

The catalyst cooler improves process unit profitability by enhancing total conversion and improving selectivity toward higher-value products such as propylene and naphtha, at the expense of gas and coke production. It is required when the unit is designed to operate in total combustion mode due to the higher heat release rate, as illustrated by the reaction enthalpy comparison below:

C + ½ O2 → CO (Partial Combustion) ΔH = - 27 kcal/mol

C + O2 → CO2 (Total Combustion) ΔH = - 94 kcal/mol

Under total combustion, regenerator temperatures can approach 760°C, raising the risk of thermal catalyst deactivation, which is mitigated by the catalyst cooler.

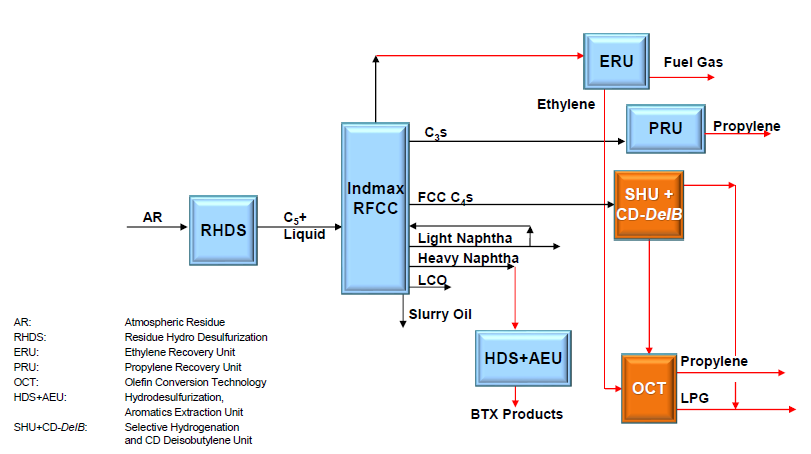

Figure 13 presents a block diagram illustrating how the petrochemical FCC unit — in this case the INDMAX™ technology by Lummus Company — can maximize petrochemical yields within the refining configuration. Another technology dedicated to maximizing olefins from residue is the R2P™ process, developed by Axens.

Figure 13 – Olefins Maximization in the Refining Hardware with INDMAX™ FCC Technology by Chevron Lummus Global Company (SANIN, A.K., 2017)

In refining configurations with conventional FCC units, beyond the higher temperature and catalyst circulation rate adjustments, it is also possible to apply zeolitic catalyst additives such as ZSM-5, which can increase olefin yields by up to approximately 9% relative to the base catalyst in some cases. While this approach increases operational costs, it can be economically attractive given the petrochemical market growth forecasts discussed above.

Hydrocracking Technologies

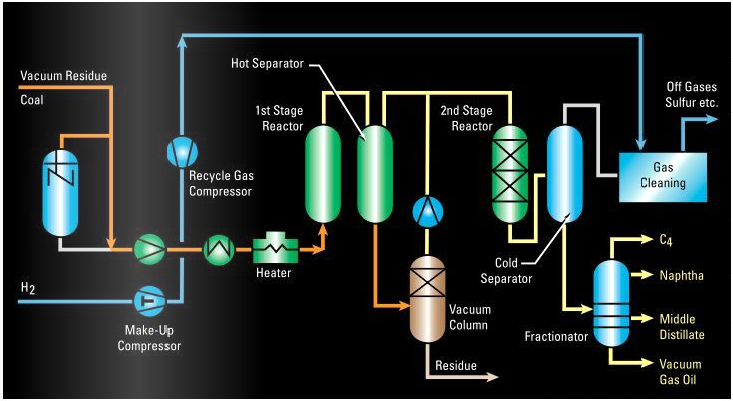

Another key technology in crude to chemicals refineries is the hydrocracking unit. Despite their high performance, fixed-bed hydrocracking technologies may not be economically effective for direct crude oil processing due to the risk of short operating cycles. Technologies based on ebullated bed reactors with continuous catalyst replacement address this limitation, enabling longer operating campaigns and higher conversion rates. The principal commercial technologies in this category include:

- H-Oil™ and Hyvahl™ (Axens Company)

- LC-Fining™ (Chevron Lummus)

- Hycon™ (Shell Global Solutions)

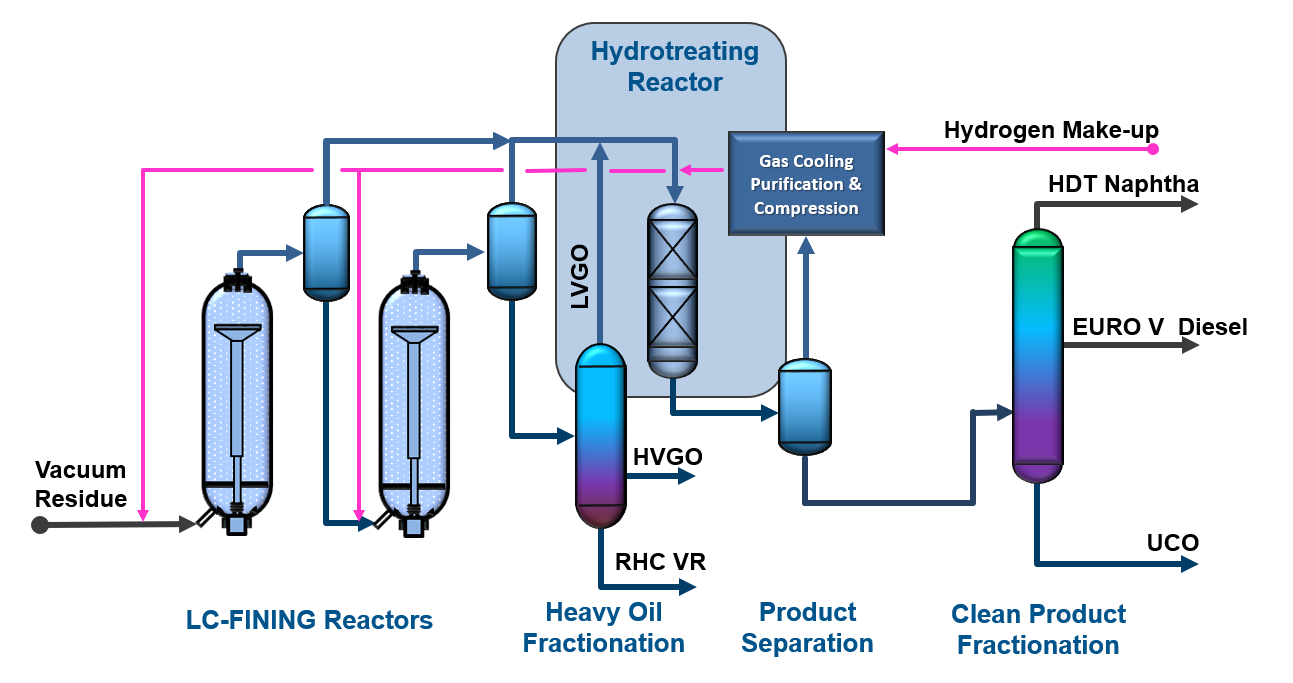

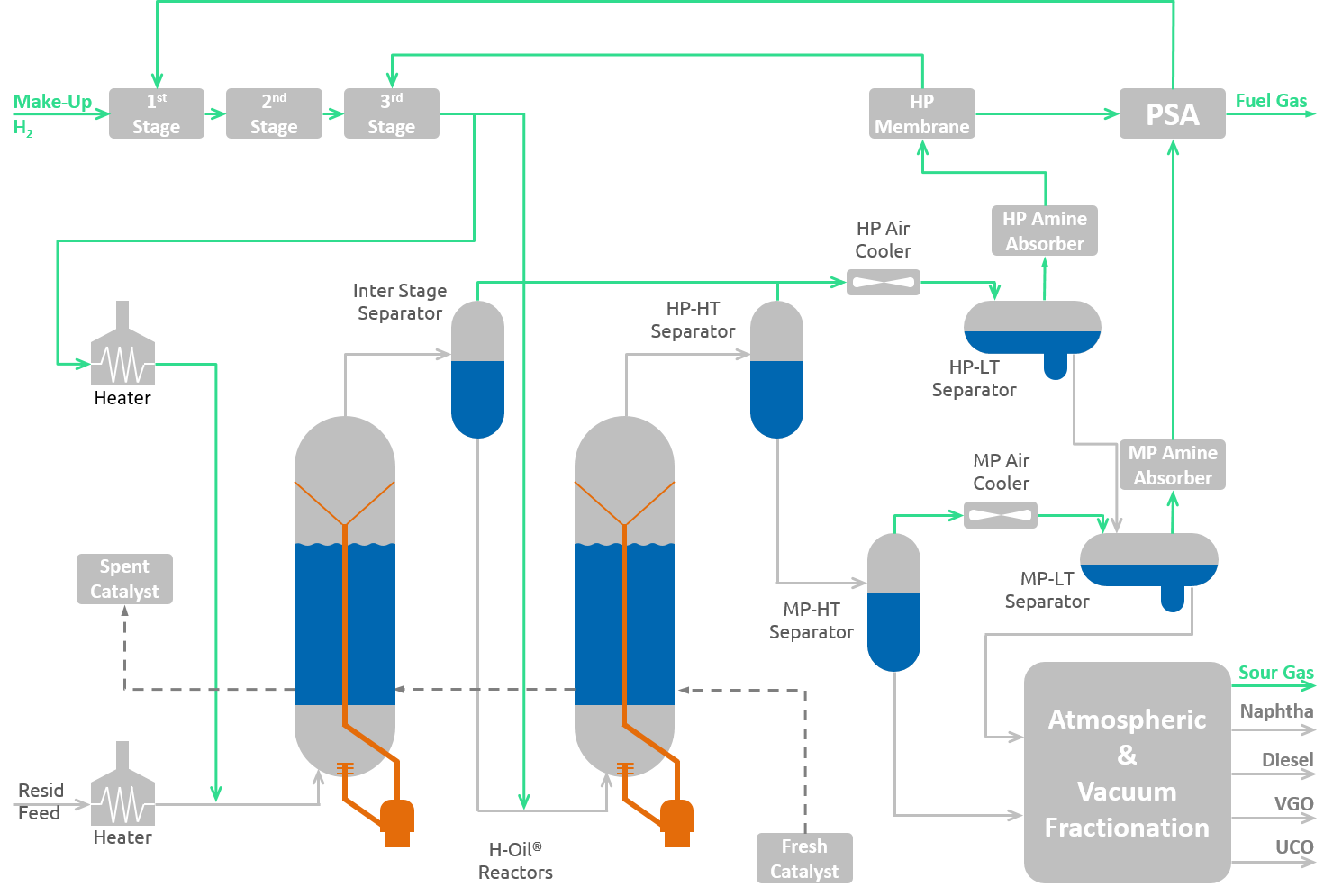

These reactors operate at temperatures above 450°C and pressures up to 250 bar. Figure 14 presents a typical process flow diagram for the LC-Fining™ process by Chevron Lummus, while the H-Oil™ process by Axens is presented in Figure 15.

Figure 14 – Process Flow Diagram for LC-Fining™ Technology by CLG Company (MUKHERJEE & GILLIS, 2018)

Catalysts applied in hydrocracking processes can be amorphous (alumina and silica-alumina) or crystalline (zeolites), and exhibit bifunctional characteristics — cracking reactions occur at the acid sites while hydrogenation reactions occur simultaneously at the metal sites.

Figure 15 – Process Flow Diagram for H-Oil™ Process by Axens Company (FRECON et. al, 2019)

Slurry phase reactors represent a further advancement over ebullated bed technologies, achieving conversions exceeding 95%. The principal commercial technologies available include:

- HDH™ (Hydrocracking-Distillation-Hydrotreatment), developed by PDVSA-Intevep

- VCC™ — VEBA-Combicracking Process, commercialized by KBR Company

- EST™ — Eni Slurry Technology, developed by ENI (Italy)

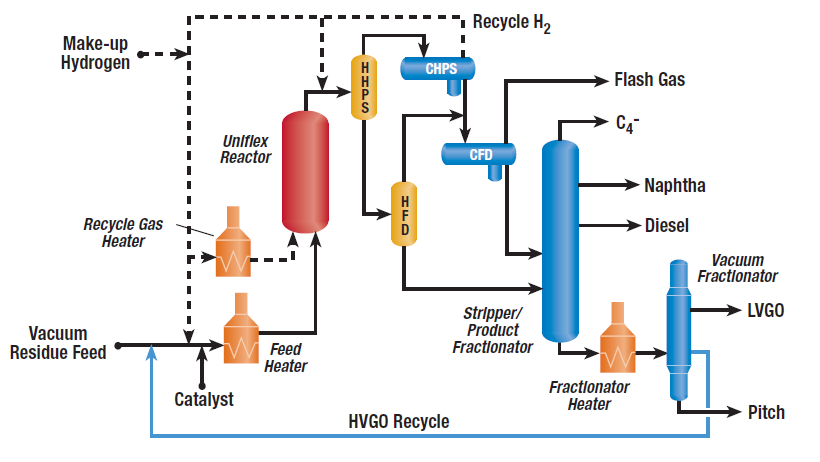

- Uniflex™, developed by UOP Company

- LC-Slurry™, developed by Chevron Lummus Company

- Microcat-RC™, developed by ExxonMobil Company

In slurry phase hydrocracking units, the catalyst is injected with the feedstock and activated in situ while reactions are carried out in slurry phase reactors — minimizing catalyst reactivation issues and ensuring both higher conversions and longer operating lifecycles. Figure 16 presents the basic process arrangement for the VCC™ technology by KBR, while Figure 17 presents the process flow diagram for the Uniflex™ technology by UOP.

Figure 16 – Basic Process Arrangement for VCC™ Slurry Hydrocracking by KBR Company (KBR Company, 2019)

Figure 17 – Process Flow Diagram for Uniflex™ Slurry Phase Hydrocracking Technology by UOP Company (UOP Company, 2019).

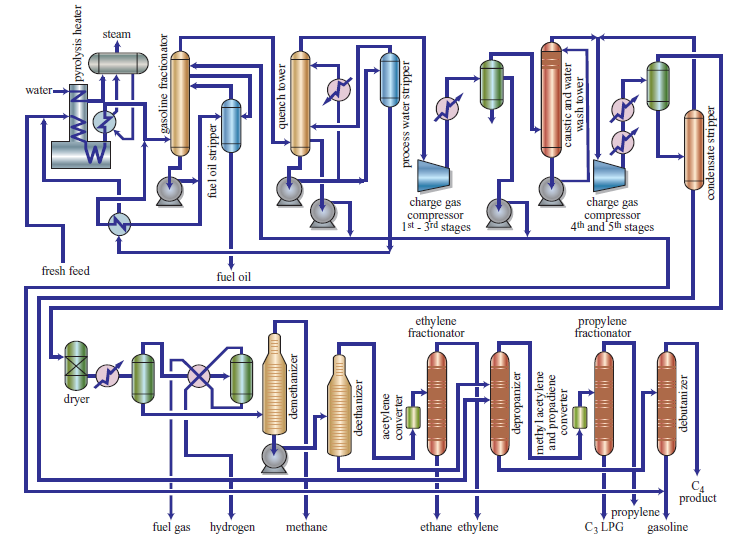

Steam Cracking

The steam cracking process plays a fundamental role in the petrochemical industry. Currently, the majority of global light olefin production — ethylene and propylene — is produced via the steam cracking route. The process consists of thermal cracking of gaseous or naphtha feedstocks to produce olefins.

Naphtha used as steam cracker feedstock is composed primarily of straight-run naphtha from crude oil distillation units. To meet petrochemical naphtha specifications, the stream must typically present a high paraffin content (above 66%). Figure 18 presents a typical steam cracking unit using naphtha as feedstock.

Figure 18 – Typical Naphtha Steam Cracking Unit (Encyclopedia of Hydrocarbons, 2006)

Given its strategic importance, major technology developers have dedicated sustained efforts to improving steam cracking technologies over the years — particularly with regard to cracking furnace design. Companies including Stone & Webster, Lummus, KBR, Linde, and Technip have each developed proprietary steam cracking process technologies. Notable commercial examples include:

- SRT™ (Short Residence Time, Lummus): Applies reduced residence time to minimize coking and extend operational lifecycle

- SCORE™ (KBR/ExxonMobil): Combines a selective steam cracking furnace with a high-performance olefins recovery section

Cracking reactions occur within the furnace tubes. The primary limitation on operating lifecycle is coke formation in those tubes. Reactions are carried out at high temperatures — between 500°C and 700°C depending on feed characteristics (inlet temperature). For heavier feeds such as gas oil, lower temperatures are applied to minimize coke formation. The combination of high temperatures and short residence time is the defining characteristic of the steam cracking process.

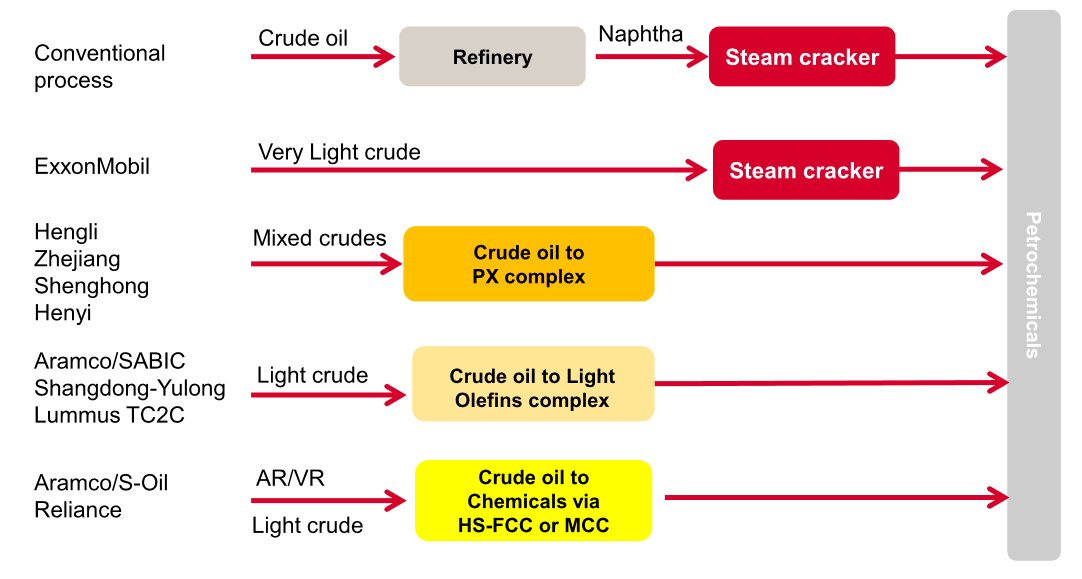

Crude to Chemicals Processing Routes

At present, three technically available processing routes are being considered for capital investment in COTC refining complexes. Figure 19 presents these concepts, based on information from S&P Global Commodity Insights.

Figure 19 – Crude to Chemicals Concepts (S&P Global Commodities Insights Company, 2024)

- Conventional integrated route: Crude oil is processed through a conventional refinery, producing petrochemical intermediates such as naphtha, which is then supplied to petrochemical assets such as a steam cracking unit

- ExxonMobil direct feed route: Selected crude oils — typically light and low in contaminants — are fed directly to petrochemical assets, bypassing conventional refining steps

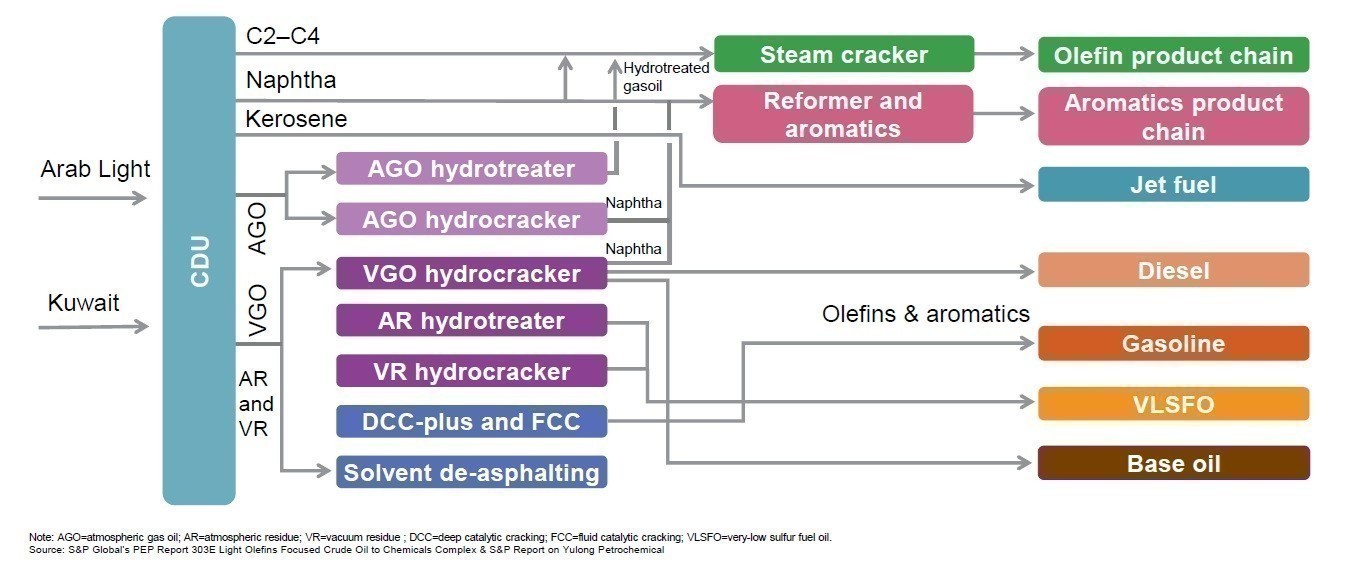

- Chinese PX-focused route (e.g., Hengli, Zhejiang Shenghong Hengyi): Mixed crude slates are processed in integrated complexes oriented toward para-xylene production, serving China's large domestic demand for light aromatics (BTX)

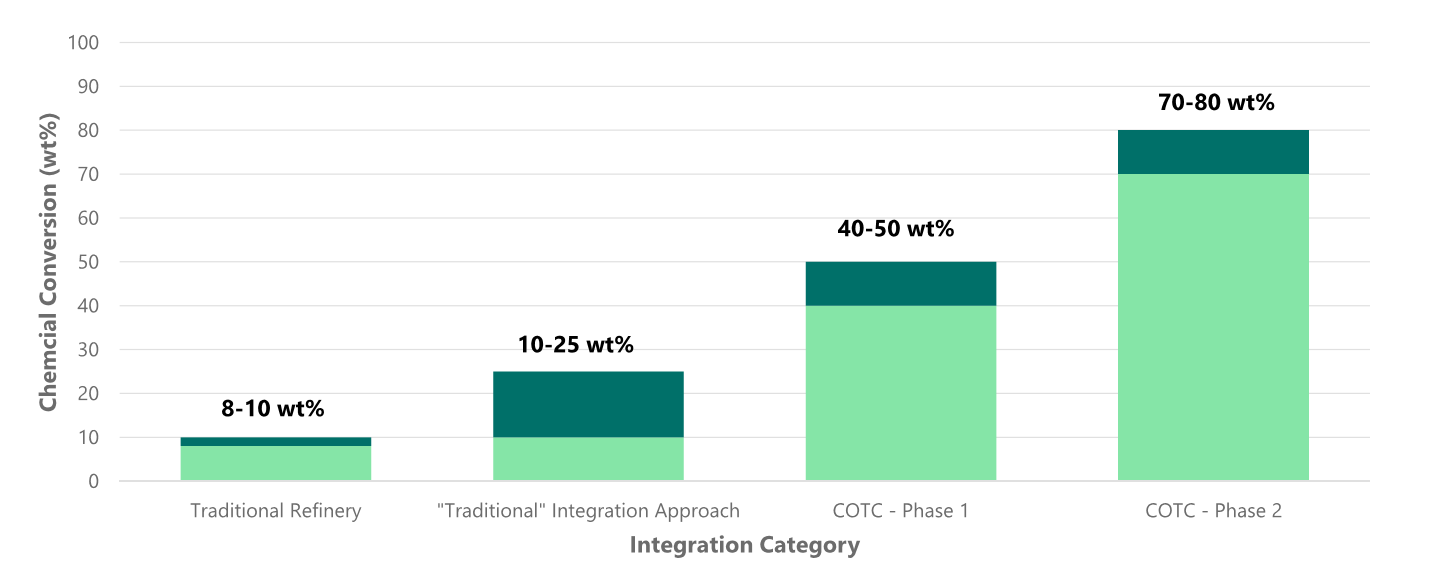

A conventional, highly integrated refining configuration is capable of achieving 15–20% petrochemicals yield, while a crude to chemicals refinery can reach up to 40%, as shown in Figure 20 according to Wood Company data. The Aramco/SABIC concept is based on a high-complexity refining configuration designed to process selected light crude oils and maximize the yield of petrochemical intermediates, primarily light olefins.

Figure 20 – Petrochemicals Yield Comparison (Wood Company, 2024)

While the advantages of closer integration between refining and petrochemical assets are compelling, it is important to recognize that downstream industry players are currently navigating a transition period. As shown in Figure 1, transportation fuels still account for a significant share of revenues. In this business context, a carefully designed transition strategy is required — one in which the economic sustainability generated by the current business model (transportation fuels) is progressively reinvested to build the future (petrochemicals maximization). Focusing exclusively on the present or exclusively on the future both represent potentially costly strategic errors.

Integrated COTC Refinery Configurations

As noted above, several technology developers are dedicating resources to developing commercial crude to chemicals refinery configurations. Figure 21 presents the COTC concept by Chevron Lummus Company, while Figure 22 presents an alternative arrangement by the same company that incorporates a delayed coking unit for residue upgrading — both aimed at maximizing petrochemical intermediate output.

Figure 21– Crude to Chemicals Concept by Chevron Lummus Company (Chevron Lummus Global Company, 2019)

Figure 22 – Crude to Chemicals Concept by Chevron Lummus Company (Nexant Company, 2018)

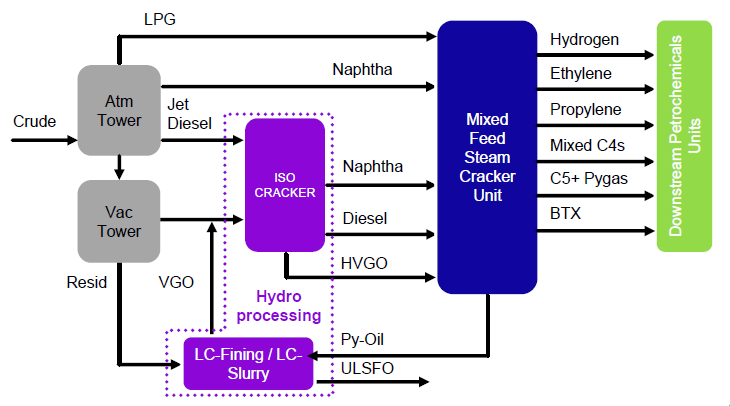

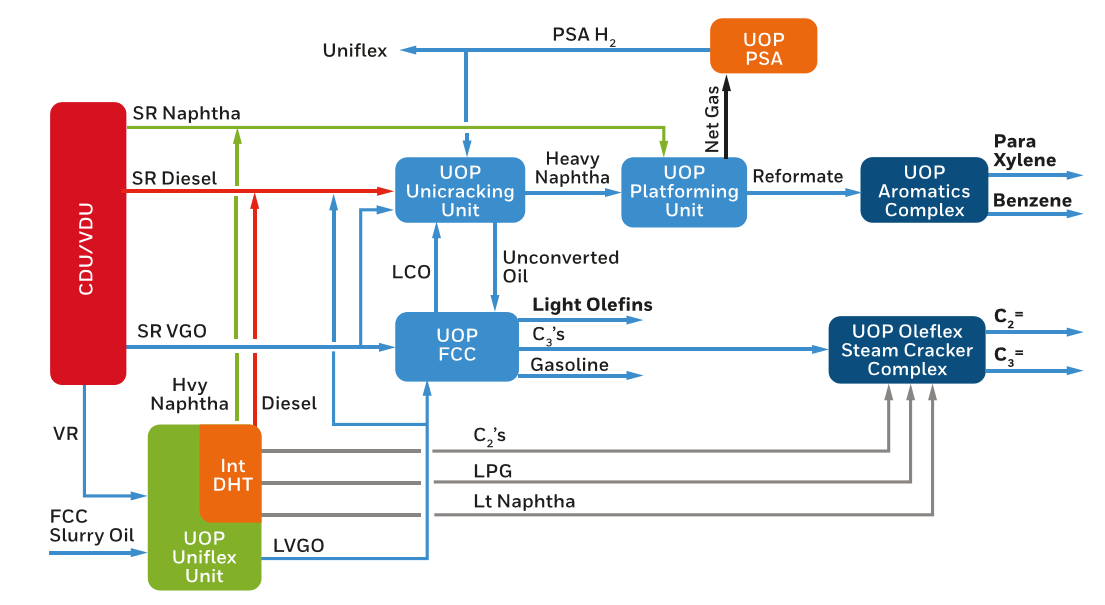

Other major refining technology developers — including UOP, Shell Global Solutions, ExxonMobil, Axens, and others — are also actively developing COTC technologies, further reinforcing that this is a defining trend in the downstream market. Figure 23 presents a highly integrated refining configuration capable of converting crude oil to petrochemicals, developed by UOP Company.

Figure 23 – Integrated Refining Configuration Based in Crude to Chemicals Concept by UOP Company.

As illustrated in Figure 23, the production focus shifts entirely toward maximizing value addition from crude oil through the production of high-value petrochemical intermediates and general-purpose chemicals, resulting in minimum fuel production.

As previously noted, major players such as Saudi Aramco have been making substantial investments in COTC technologies, aiming to achieve even greater integration between their refining and petrochemical assets and significantly strengthening their competitive position in the downstream market. The major technology licensors — Axens, UOP, Lummus, Shell, ExxonMobil, and others — have likewise committed resources to developing technologies enabling closer downstream integration, allowing refiners to extract maximum added value from processed crude — an increasingly critical requirement in a margin-compressed environment.

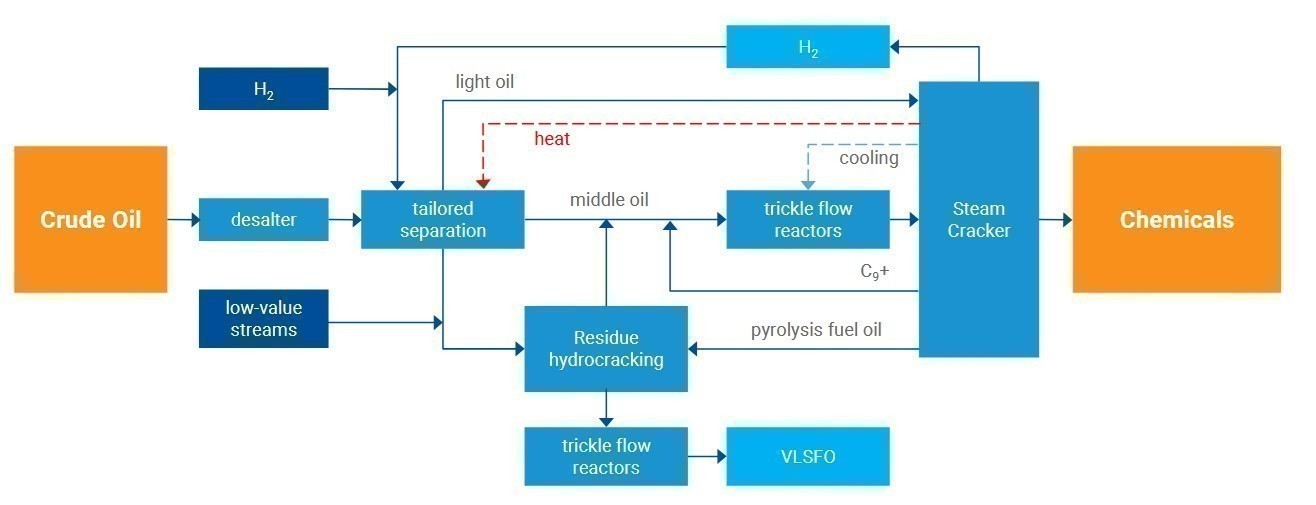

Lummus Company recently announced the commercial implementation of its proprietary TC2C™ (Thermal Crude to Chemicals) technology by a major Asian downstream operator, further reinforcing the growing COTC trend in the Asian market. According to the licensor, the TC2C™ process can achieve a yield of 70% by mass of high-value petrochemicals from light crude feedstocks. Figure 24 presents a block diagram for this technology.

Figure 24 – Block Diagram for the TC2C™ Crude to Chemicals Technology by Lummus Company

Capital Investment Trends and Competitive Implications

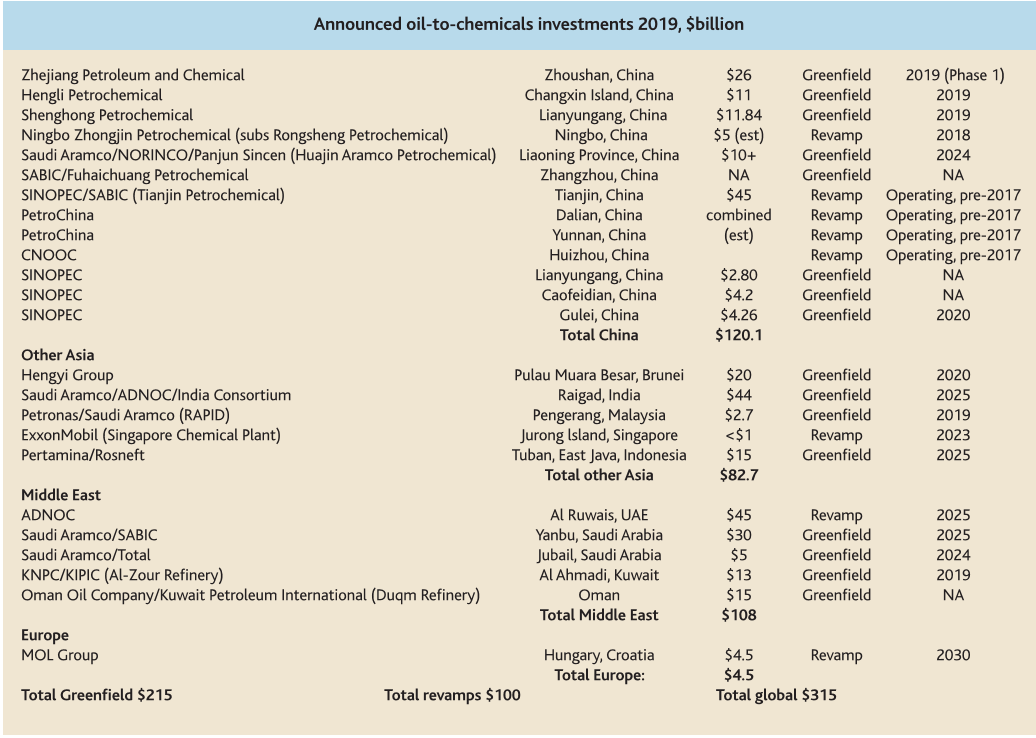

Based on data from The Catalyst Group (TCGR), as of 2019 there were significant capital investments underway in crude to chemicals projects, as summarized in Table 2.

Table 2 – Crude Oil to Chemicals Investments (The Catalyst Group, 2019)

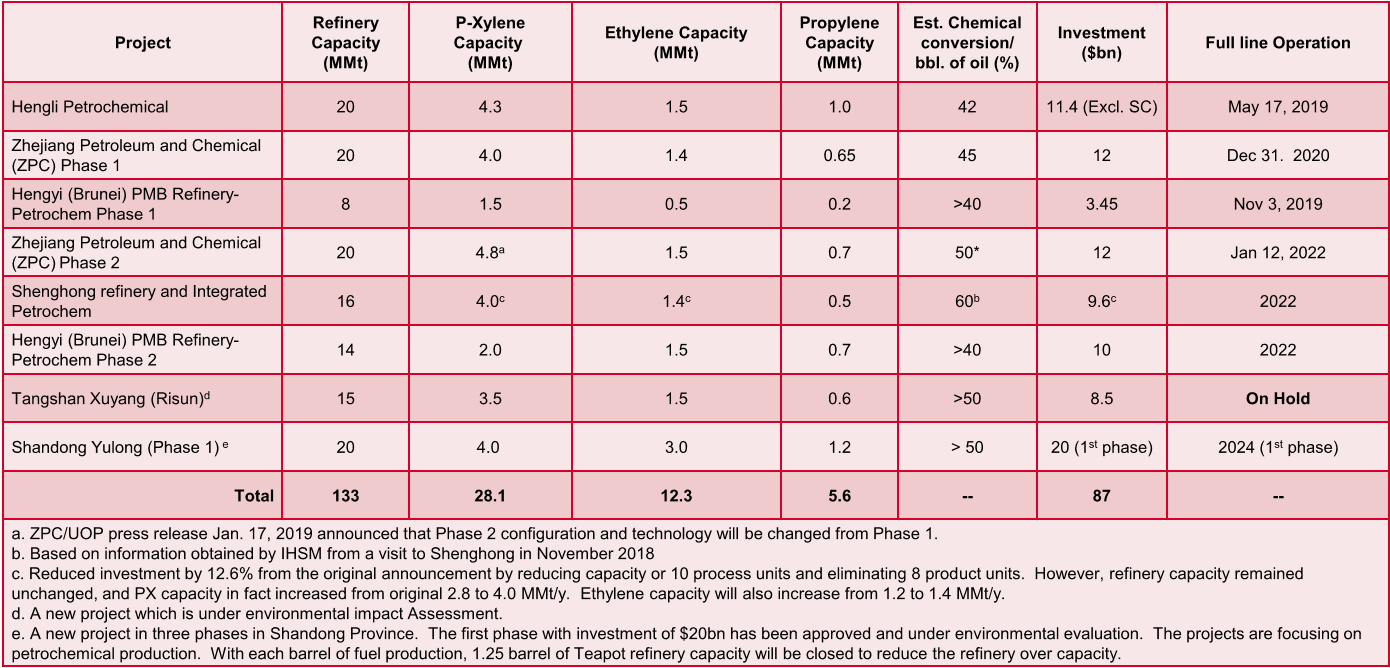

It is expected that some of these investments were delayed as a result of the economic crisis caused by the COVID-19 pandemic. Nevertheless, the data firmly reinforce the market trend. Notably, close to 64% of global crude to chemicals investment is concentrated in Asia, predominantly among Chinese players. Considering only petrochemical complexes focused on para-xylene (PX) production, total committed capital investment amounts to approximately USD 87 billion, as detailed in Table 3.

Table 3 – PX focused Crude to Chemicals Capital Investments (S&P Global Commodity Insights, 2024)

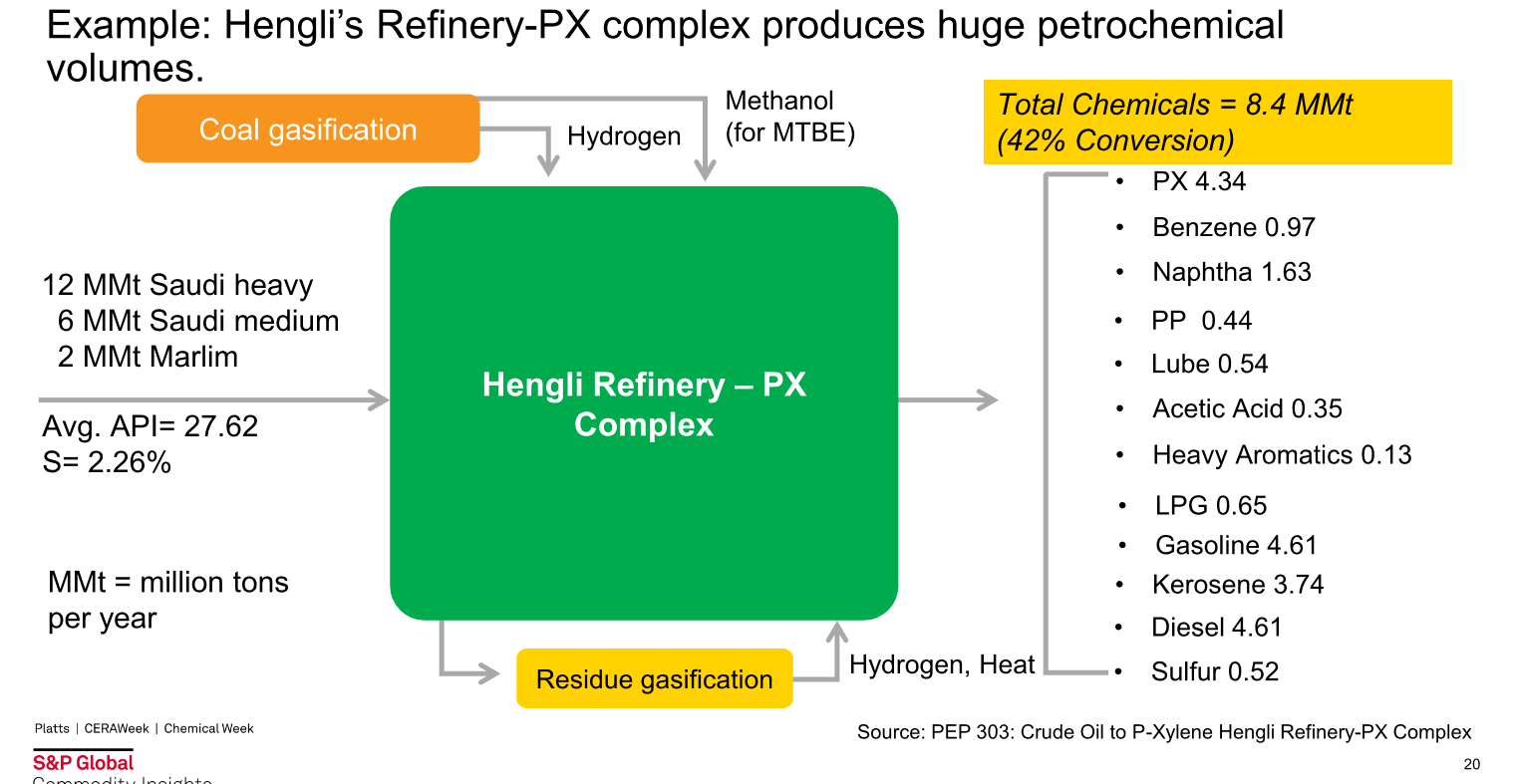

Analyzing Figure 25, the significantly higher value-added output achieved in COTC refineries is evident, even when compared with highly integrated conventional refineries. Figure 24 presents a real-world example of the high petrochemical yields achievable in a COTC refinery — in this case the Hengli Petrochemical Complex in China.

Figure 25 – Petrochemicals Yield for the Hengli Crude to Chemicals Complex (S&P Global Commodity Insights, 2024)

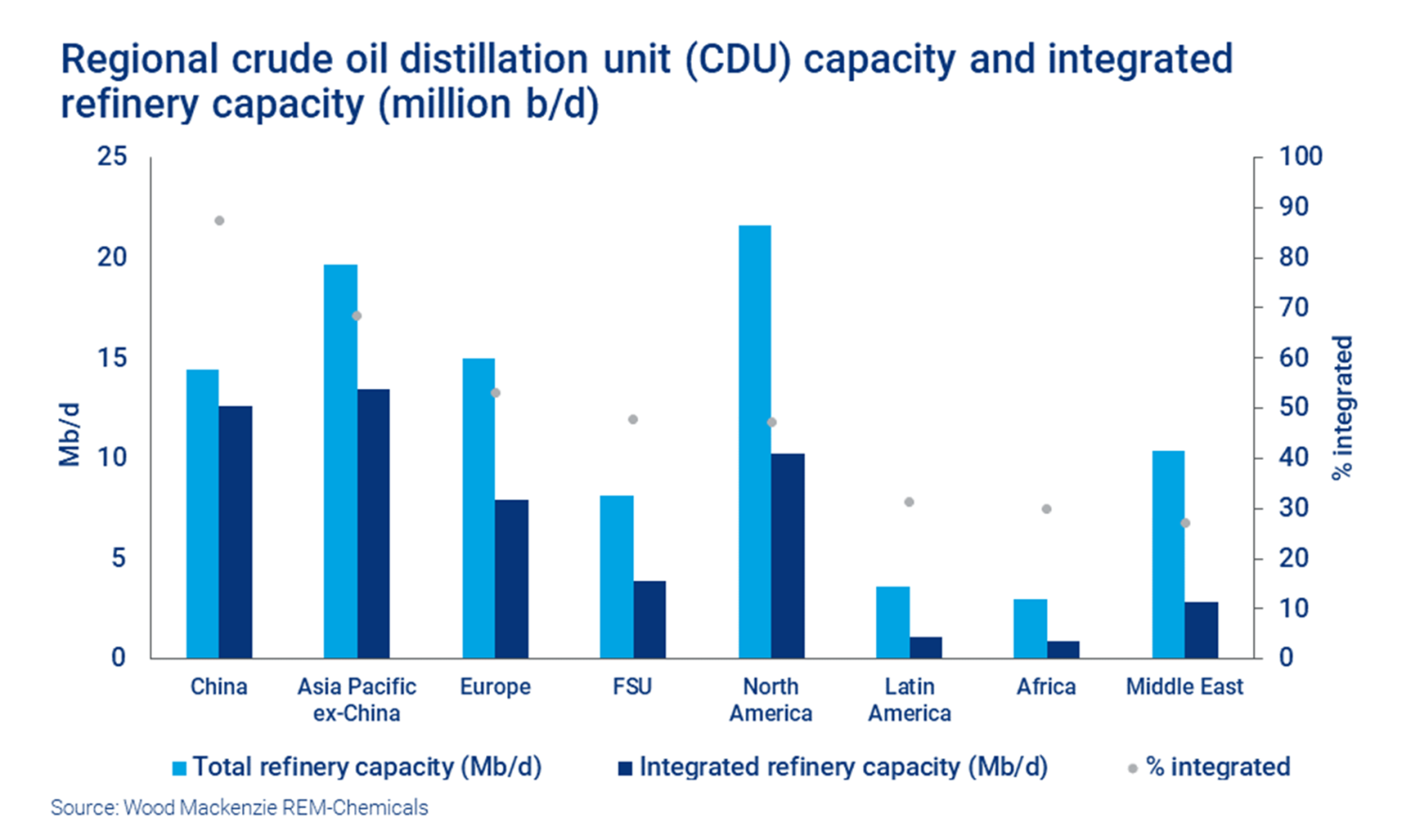

It is worth highlighting the potential competitive imbalance emerging in the downstream sector in the near term, driven by growing petrochemical demand. Based on 2019 data, total capital investment in COTC refineries amounts to USD 300 billion, with 64% concentrated in Asia. Figure 26 reinforces this point by comparing crude oil distillation capacity with integrated refinery capacity for each continent.

Figure 26 – Crude Oil Distillation Capacity and Integrated Refinery Capacity for Each Continent (Wood Mackenzie, 2023)

Figure 26 shows that the Asian players have a superior integration capacity of their refining assets in comparison with another continents, as mentioned above, this can be translated in a significant competitive advantage to the Asian players and a great potential o competitive imbalance of the downstream market considering the recent forecasts which indicates growing demand for petrochemicals. Furthermore, it’s possible to see the power of the China in the Asian and global downstream market.

As aforementioned, face the current trend of reduction in transportation fuels demand at the global level, the capacity of maximum adding value to crude oil can be a competitive differential to refiners. Due to the high capital investment needed for the implementation that allows the conventional refinery to achieve the maximization of chemicals, capital efficiency becomes also an extremely important factor in the current competitive scenario as well as the operational flexibility related to the processed crude oil slate.

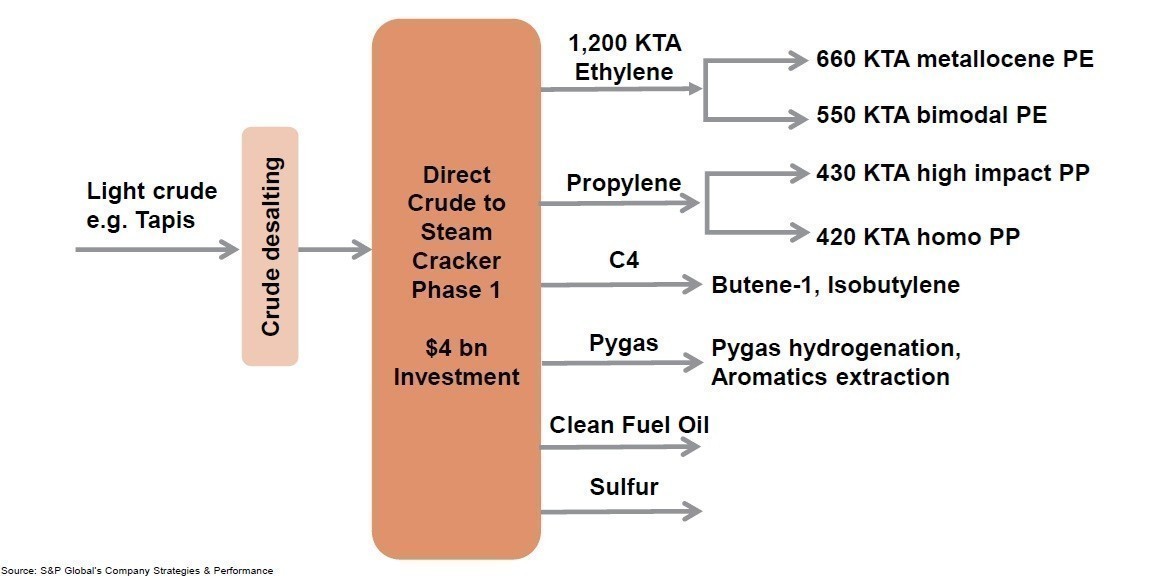

Still according to S&P Global, further capital investments in COTC refining assets in China are planned. Figure 27 presents the concept of the planned ExxonMobil Huizhou Phase 1 project.

Figure 27 - Concept of ExxonMobil Huizhou Phase 1 project (S&P Global Commodities Insights Company, 2026)

The ExxonMobil Huizhou Phase 1 project is expected to start up in 2026, further strengthening the competitive positioning of Chinese players in the global petrochemical market and adding to the pressure on other market participants — particularly European producers operating at higher costs. Another significant COTC investment in China is the Shandong Yulong Integrated Petrochemicals Phase 1 project, which is focused on both aromatics and light olefins and includes two world-scale mixed-feed steam cracker trains, as presented in Figure 28.

Figure 28 - Concept of Shangdong Yulong Integrated Petrochemicals Phase-1 project (S&P Global Commodities Insights Company, 2026)

Consequences of the Competitive Imbalance - The wave of Steam Cracking Closures in Europe

According to recent data from Stratas Advisors, a reduction in European steam cracking processing capacity of approximately 5.7 million metric tons per year (MMtpy) is expected between 2024 and 2026 due to permanent shutdowns.

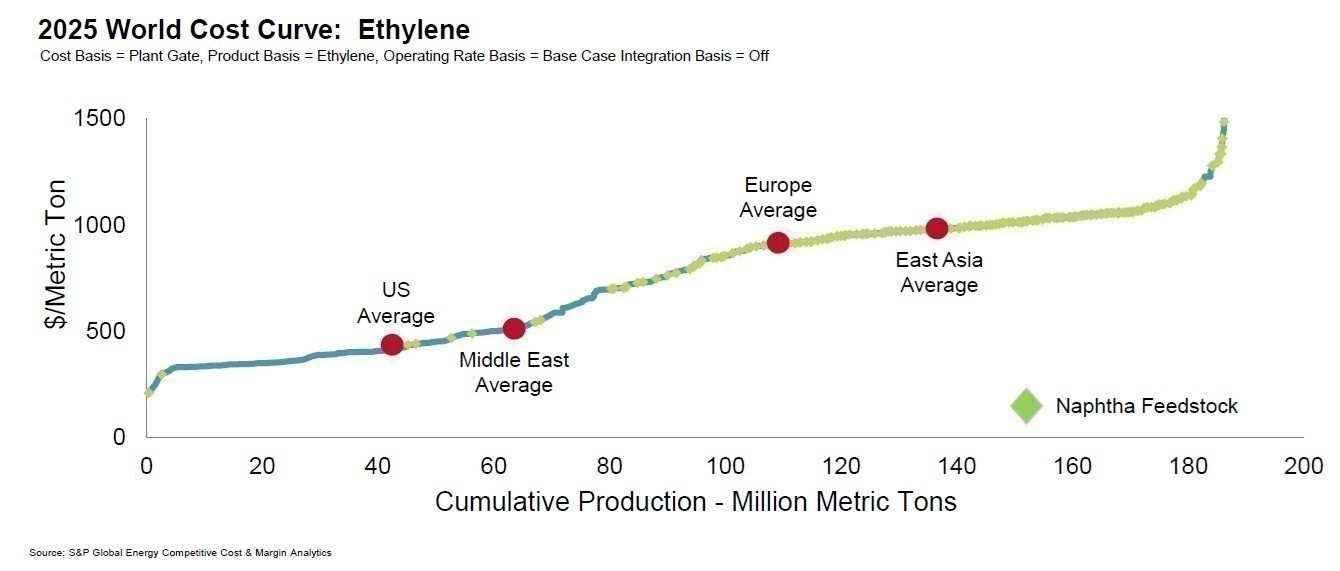

The primary driver of poor competitiveness among European operators is feedstock cost: the majority of European steam crackers use naphtha as feedstock, which is significantly more expensive than the ethane and LPG used by US and Middle Eastern operators. The latter regions benefit from abundant availability of these lighter feedstocks at relatively low cost, enabling the operation of more modern and efficient crackers. Figure 29 illustrates the cost disadvantage faced by European players relative to US and Middle Eastern producers.

Figure 29 - Ethylene Production cost curve - (S&P Global Commodities Insights Company, 2026)

A large proportion of Chinese steam crackers also operate on naphtha, but their integration within large-scale, modern COTC complexes provides significant economies of scale and operational efficiency — placing them in a structurally stronger competitive position than their European counterparts.

As previously noted, further capital investment in COTC refining assets in China is planned. The combination of feedstock cost disadvantages, global oversupply of petrochemical intermediates — which demands ever-greater efficiency from all market participants — and the continued expansion of large-scale integrated COTC refineries in China places European players under intensifying competitive pressure.

Conclusion

Today, it remains difficult to envision a global energy matrix free of fossil transportation fuels, particularly in developing economies. Nevertheless, recent market forecasts, growing demand for petrochemicals, and persistent pressure to reduce the environmental impact of fossil fuels collectively create a positive and sustained driving force for closer integration between refining and petrochemical assets. In the most advanced scenario, zero-fuels refineries are expected to grow in prevalence over the medium term, particularly in developed economies.

The synergy between refining and petrochemical processes increases the availability of raw materials for petrochemical plants and improves energy supply reliability, while simultaneously delivering better refining margins to refiners — reflecting the inherently higher added value of petrochemical intermediates relative to transportation fuels. The development of COTC technologies reinforces the necessity for brownfield refineries to pursue closer refining-petrochemical integration in order to compete in a market increasingly centered on petrochemicals rather than fuels. It is important to note the natural competitive advantage of Middle Eastern refiners, who benefit from easy access to the light crude oils best suited to COTC processing schemes.

Using the Blue Ocean Strategy framework, the transportation fuels market increasingly resembles the red ocean: low margins, intense competition, and limited differentiation capacity. The petrochemicals sector, by contrast, functions as the blue ocean — accessible to fewer players operating under competitive conditions, offering higher refining margins and significant differentiation from fuel-focused refiners. Market forecasts consistently confirm that refiners capable of maximizing petrochemical yields at the expense of transportation fuels are positioned for superior near-term economic performance. COTC technologies represent the most advanced expression of this positioning, offering even greater competitive advantage to refiners with the capital investment capacity to implement them.

At the extreme end of the integration spectrum are the zero-fuels refineries. As noted, it is still difficult to envision the downstream market without transportation fuels, but this appears to be a serious structural trend — one that downstream players must incorporate into their strategic planning, treating it simultaneously as both opportunity and threat. Even operators with more limited capital resources can take targeted actions to maximize petrochemical yields within their existing refining configurations. Disruption remains a significant undertaking in the downstream industry, but COTC refining assets have the potential to produce a structural competitive imbalance — particularly given the concentration of capital investment in the Asian market. The downstream industry has a long history of adapting to evolving crude consumption patterns; the evolution toward crude to chemicals represents the next chapter in that progression, aimed at extracting the maximum possible added value from processed crude — with petrochemical yields exceeding 70%.

Reinforcing the COTC trend at the highest level of the industry, SABIC has announced its intention to invest in a new crude to chemicals refinery with a capacity of 400,000 barrels per day. Separately, SATORP — a joint venture between TotalEnergies and Aramco — announced USD 11 billion in capital investment in the Amiral petrochemical complex, aimed at promoting closer integration with the Jubail refinery in Saudi Arabia. These announcements further confirm the broad industry trend toward refining-petrochemical integration in order to maximize the added value extracted from processed crude.

Less integrated refiners tend to compete in a red ocean environment where refining margins are lower, reflecting the lower added value generated from transportation fuels, high-sulfur fuel oil, and asphalt. Despite this, economic sustainability remains achievable depending on local market characteristics — in which case capital discipline and operational efficiency become even more critical for these players.

In our view, the current global petrochemical oversupply crisis is a natural consequence of the massive capital investment program undertaken by Chinese players in COTC refining assets — which has generated substantial production capacity and scale economies capable of dramatically reducing production costs relative to other market participants. The broader trend among refiners toward closer refining-petrochemical integration, driven by the increasingly hostile environment for fossil fuels, has led capital-rich players to make significant changes to their refining assets in order to maximize chemicals at the expense of fuels. Having built a refining park with exceptional petrochemical production potential, Chinese operators have in effect gained structural control of a significant share of the global petrochemical market. On the other side, less competitive players — as appears to be the case for European producers — must urgently seek solutions to improve efficiency and scale in order to achieve a more sustainable competitive position.

#cotc #crudeoiltochemicals #c2c #petrochemicalintegration #refiningassets #hydrocracking #steamcracking #integratedrefinery #crudetochemicals