The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

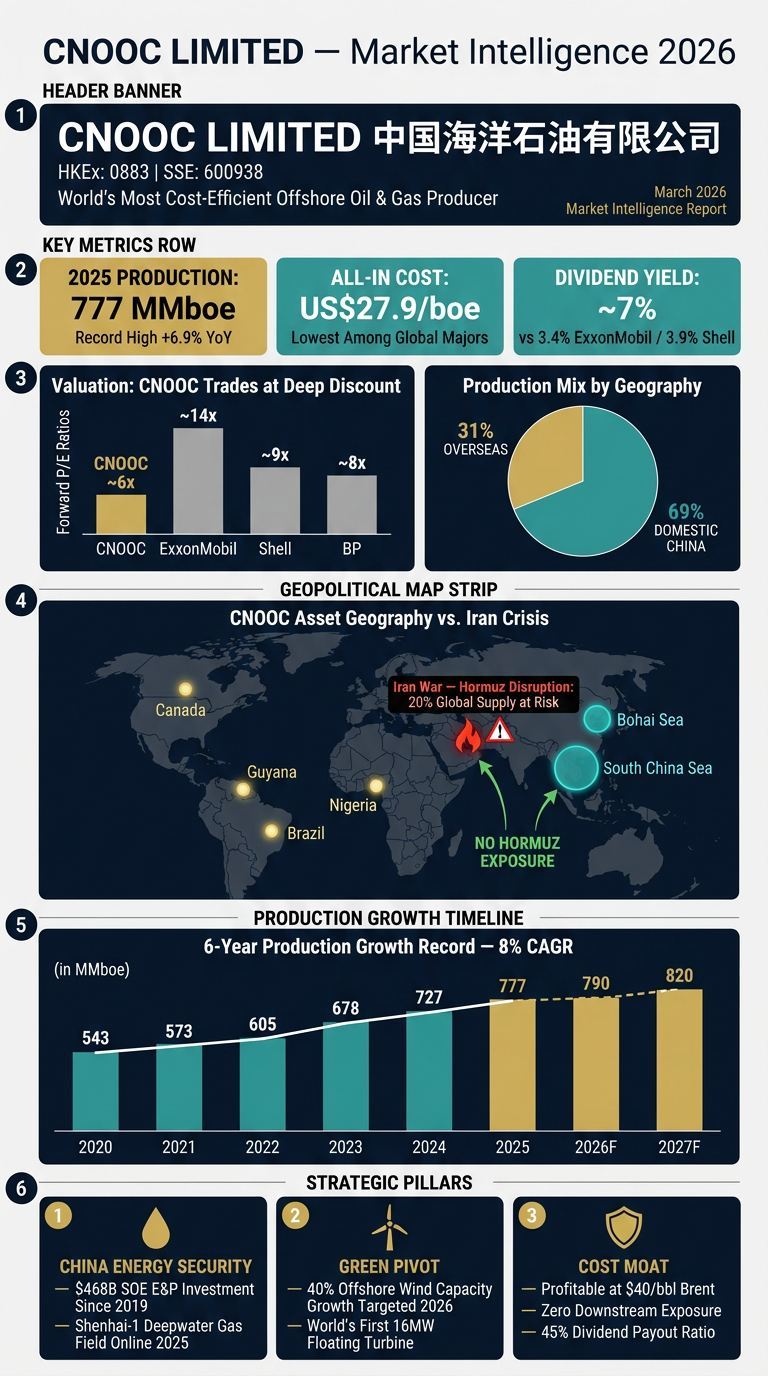

March 2026 | Based on 2025 Full-Year Results and Current Market Conditions

CNOOC Limited (HKEx: 00883; SSE: 600938) stands as the world's most cost-efficient publicly listed offshore oil and gas producer — and one of the most compelling equity stories in the global energy sector. Its share price has surged +35.68% year-to-date in 2026 alone, propelled by a constellation of reinforcing factors: record production volumes, industry-leading cost discipline, China's accelerating energy self-sufficiency drive, and a geopolitical shock of historic proportions — the U.S.-Israel war on Iran, which has driven Brent crude above $100/barrel and simultaneously disrupted approximately 20% of global oil supply.

Despite a 14.6% decline in average Brent prices during 2025 that squeezed net profit to RMB122.1 billion (-11.5% YoY), CNOOC achieved record net production of 2.13 million BOE per day. This paradox — falling profits on record output — actually validates rather than undermines the investment thesis: CNOOC's structural cost advantage kept the company highly profitable at $68/bbl Brent when most Western peers struggled. With Brent now trading near $95-106/bbl and climbing, and with the company's production still growing, the conditions for a sustained re-rating are firmly in place.

Record Output, Profit Resilience

CNOOC has recorded production growth for six consecutive years, with a five-year compound annual growth rate (CAGR) of approximately 8%. Key 2025 results include:

| Metric | 2024 | 2025 | Change |

|---|---|---|---|

| Net production (MMboe) | 726.8 | ~777 (2.13 MMboe/d) | +6.9% |

| Net profit (RMB bn) | 137.9 | 122.1 | -11.5% |

| Oil & gas sales revenue (RMB bn) | ~420 | 335.7 | -11.4% |

| All-in cost (US$/boe) | 28.52 | 27.9 | -2.2% |

| Annual dividend (HK$/share) | 1.40 | 1.28 | -8.6% |

| Dividend payout ratio | 45% | 45% | Stable |

The headline profit decline masks the deeper narrative: it was almost entirely attributable to a 14.6% YoY fall in realized Brent crude prices, not to operational weakness. CNOOC actually reduced its all-in cost by 2.2% to US$27.9/boe in a year of price headwinds — a feat that speaks directly to management discipline and structural advantages in its offshore portfolio.

The Cost Moat: Why US$27.9/boe Is a Structural Advantage

CNOOC's all-in cost of US$27.9/boe is the lowest among major listed oil producers globally. This is not a cyclical achievement but a structural one rooted in three factors:

Offshore-only E&P focus: CNOOC has no downstream refining or chemicals burden to cross-subsidize. Every barrel produced goes straight to the income statement at full upstream margin.

Chinese offshore basin advantages: The Bohai Sea, South China Sea, and East China Sea offer high-density, large-scale fields with relatively short subsea tiebacks to onshore infrastructure — low lifting costs vs. global deepwater averages.

Absence of legacy onshore depletion costs: Unlike PetroChina or Sinopec, CNOOC carries no aging onshore field portfolio requiring expensive enhanced recovery.

At US$27.9/boe, CNOOC is profitable even if Brent falls to approximately $40/bbl — a margin of safety that no Western major can match. ExxonMobil's equivalent all-in cost is estimated above $40/boe; Shell's upstream breakeven is even higher.

Revenue Architecture

CNOOC's revenue is almost entirely upstream — oil and gas sales accounted for RMB335.7 billion in 2025, representing ~95%+ of total revenues. This pureness of form is a double-edged sword: it provides maximum leverage to oil price upside but also maximum exposure to price downturns, reflected in the 11.5% profit decline during 2025's softer price environment.

The production mix is increasingly diversified by geography and increasingly weighted toward natural gas:

By geography: 69% domestic (China), 31% overseas

Natural gas growth: Gas production rose +12.0% in H1 2025 and +11.6% in 9M 2025, materially outpacing crude oil growth and reflecting deliberate portfolio rebalancing toward lower-carbon hydrocarbons

Key domestic contributors: Shenhai-1 (South China Sea deepwater, commissioned at full capacity June 2025 with 15 MMm³/day peak output), Bozhong 19-2, Kenli fields

Key overseas contributors: Guyana Yellowtail (Stabroek block), Brazil Mero 3, Canada (Long Lake SAGD), Nigeria, and a new exploration block in Kazakhstan signed H1 2025

Gas as the Strategic Growth Vector

The acceleration of natural gas production is not accidental. CNOOC is executing Beijing's directive to expand domestic gas supply — a strategic priority made urgent by the 2022 global LNG shock and the ongoing vulnerability created by the Iran war's effect on Qatar (QatarEnergy suspended LNG production following an Iranian drone attack, disrupting 20% of global LNG supply). Shenhai-1 alone, with proven reserves exceeding 150 billion cubic meters and all 23 subsea wells now operational, is a landmark achievement in Chinese deepwater gas development. Gas output directly supplies the Guangdong-Hong Kong-Macao Greater Bay Area — strategically insulating China's most economically critical industrial region from import dependency.

The Strategic Imperative

The single most important long-term driver for CNOOC is a state-level strategic imperative: China's push to reduce its vulnerability to external supply disruptions through maximum domestic resource development. Four primary factors drive this strategy — economic security, geopolitical risk mitigation, supply chain resilience, and long-term cost optimization. Chinese SOEs (CNPC, Sinopec, CNOOC) have collectively invested approximately $468 billion in exploration and production since 2019 — a 25% increase over the prior six-year period.

CNOOC sits at the operational heart of this strategy. China's new five-year plan (2026–2030) targets annual oil production of at least 200 million metric tons (4 MMbpd) and continued gas growth through 2030. The country is simultaneously building 11 new strategic oil reserve sites with 169 million barrels of combined storage capacity across 2025 and 2026 — the equivalent of two weeks of China's crude imports — with CNOOC among the operators.

Why CNOOC Is Irreplaceable in This Strategy

Of China's three major NOCs, CNOOC is the one with the most direct mandate for offshore and deepwater development — the last major frontier for Chinese domestic resource growth. The South China Sea alone holds an estimated 11 billion barrels of oil and 31.2 billion BOE of natural gas in proved and probable reserves. China's discovery of the Lingshui 36-1 gas field (>100 billion m³) in August 2024 and Shenhai-1's full commissioning in 2025 demonstrate that this frontier is now yielding commercial-scale results.

CNOOC's pipeline network has expanded beyond 10,000 km with plans to reach 13,000 km — building the arterial infrastructure that ties offshore production to onshore demand centers. This physical infrastructure moat deepens with every new field brought online.

The Iran War Shock of 2026

The U.S.-Israel war on Iran, which commenced in early March 2026, has created what the International Energy Agency describes as "the largest supply disruption in the history of the global oil market". The immediate effects are stark:

Brent crude surged from approximately $70 to over $100/barrel — a >40% spike — the largest single-event move since the 2020 pandemic lockdowns

Iran's effective closure of the Strait of Hormuz threatens approximately 20 million barrels per day — roughly 20% of global petroleum liquids consumption

QatarEnergy suspended LNG production following Iranian drone attacks, triggering a 60% rise in LNG prices and creating acute supply anxiety for Asian importers

WTI crude briefly approached $95/barrel on March 27, 2026

Goldman Sachs warned oil could climb above $100/barrel if shipping disruptions continue

CNOOC's Asymmetric Exposure to the Upside

For CNOOC, this geopolitical disruption is a pure upstream windfall:

No refining exposure: Unlike integrated majors, CNOOC has no downstream segment to suffer from higher feedstock costs — every dollar of oil price increase flows directly to upstream margins.

No Hormuz exposure: CNOOC's primary production is in the South China Sea, Bohai Sea, Canada, Guyana, and Brazil — none of which is threatened by the Strait of Hormuz closure.

China as buyer advantage: As the world's largest crude importer, China has been diversifying supply sources away from the Middle East — further insulating CNOOC's domestic production volumes from regional disruption.

Goldman Sachs projection: Even at a moderate Brent average of $85, CNOOC's annual cash flow could increase by more than 10%. At the current $100+ levels, the uplift is substantially larger.

CICC, one of China's leading investment banks, raised its H-share target price by 22.8% to HK$28 and A-share by 29% to RMB38.8 in March 2026, maintaining Outperform ratings, citing the geopolitical premium and projected 2027 net profit of RMB142.47 billion.

Russia, Iran, and China's Supply Diversification

The fractured global energy order has paradoxically reinforced CNOOC's strategic value to Beijing. When U.S. sanctions targeted major Russian oil exporters, Chinese state companies briefly curtailed Russian crude purchases — exposing Beijing's vulnerability to any supply source operating within the Western sanctions architecture. CNOOC's offshore production, physically located within Chinese-controlled waters and operating through Chinese-domiciled entities, represents supply that is effectively sanction-proof. In a world of proliferating sanctions, this is a premium attribute that Western markets systematically undervalue when pricing CNOOC's equity.

A Structural Valuation Gap vs. Western Majors

CNOOC trades at approximately 6x forward earnings with a dividend yield above 7% — a deep discount to Western majors despite superior production growth, lower costs, and stronger reserves replacement (167% RRR in 2024).

| Company | P/E (Fwd) | Div. Yield | Production Growth | All-In Cost |

|---|---|---|---|---|

| CNOOC (HKEx: 0883) | ~6x | ~7%+ | +8% CAGR (5yr) | $27.9/boe |

| ExxonMobil (NYSE: XOM) | ~14x | 3.4% | ~2-3% | >$40/boe |

| Shell (LON: SHEL) | ~9x | 3.9% | ~1-2% | >$40/boe |

| BP (LON: BP) | ~8x | 4.5% | Flat/declining | >$45/boe |

This discount reflects several non-fundamental factors: geopolitical risk premium associated with a Chinese state-owned entity, the legacy impact of the 2021 U.S. NYSE delisting (which CEO Xu Keqiang described as having a "profound impact" on share price), restricted access for U.S.-based institutional investors, and the general discount applied to Hong Kong-listed Chinese equities. Goldman Sachs explicitly describes CNOOC as "relatively undervalued compared to developed market counterparts".

The 2022 Shanghai A-share listing was a deliberate strategic response to the NYSE delisting — tapping Chinese domestic capital markets as an alternative source of institutional depth. This strategic reorientation has been broadly successful: CNOOC's A-share (SSE: 600938) has attracted strong domestic fund inflows, partially offsetting the loss of U.S. investor access.

Production Growth Is Built In

CNOOC has 14 new projects commencing production in 9M2025 alone, and its three-year rolling production targets are underpinned by projects already under construction:

2026: 780–800 MMboe

2027: 810–830 MMboe (+5% YoY)

2030 aspiration: Continued growth as new deepwater and gas fields ramp

Stable capex of RMB125–135 billion/year means this growth is self-funded without requiring equity raises or leverage increases. The capital allocation is weighted toward high-return development (61% of capex) with disciplined exploration (16%) and production maintenance (20%).

The Green Pivot: Offshore Wind as a New Revenue Pillar

CNOOC is not content to remain a pure-play hydrocarbon company. In 2026, it targets a 40% increase in offshore wind capacity — leveraging its offshore infrastructure expertise and governmental mandate to become a major player in Chinese offshore wind. Key developments include:

Commissioning of the world's first 16MW TLP-supported floating wind turbine at the Lufeng oilfield cluster

A RMB10 billion (~$1.4B) investment to electrify Bohai Sea drilling platforms using offshore wind

Target to consume more than 1 billion kWh of green electricity in 2025 (+30% YoY), reducing operational emissions

Advancing CCS/CCUS industrialization programs, integrating carbon asset management into investment evaluation

This 10% capex allocation to clean energy is not merely greenwashing — it creates a second, long-duration revenue stream tied to China's aggressive renewable expansion targets, while simultaneously reducing CNOOC's carbon intensity and regulatory risk exposure.

Oil Price Downside

CNOOC's share price exhibits a correlation coefficient of approximately 0.9 with Brent crude prices. While the current geopolitical environment has shifted the oil price floor upward, any resolution of the Iran conflict or an OPEC+ supply surge could reverse recent price gains. BNEF estimates Brent could average $55/bbl in a benign 2026 scenario assuming no Iranian supply disruption — a 40% drop from current levels that would significantly compress CNOOC margins.

U.S. Sanctions and Western Capital Market Exclusion

CNOOC remains on the U.S. OFAC-linked Chinese military company list, barring most U.S. institutional investors from owning shares. This structural exclusion from the world's deepest capital pool permanently suppresses CNOOC's valuation relative to peers — a discount that is difficult to quantify but real. Any escalation of U.S.-China tensions could extend or deepen these restrictions.

Geopolitical South China Sea Risk

CNOOC's most important growth frontier — the South China Sea — is also its most geopolitically contested. Tensions with the Philippines, Vietnam, and the U.S. Navy over overlapping territorial claims represent a tail risk to asset integrity that does not appear in standard risk models.

Peak Oil Demand Horizon

China has pledged to achieve peak domestic oil consumption by 2030, aided by rapid EV adoption. While this timeline likely understates the durability of petroleum demand, it creates a medium-term ceiling on CNOOC's domestic market growth. The company's pivot to natural gas and offshore wind is partly a hedge against this structural transition.

CNOOC Limited combines a rare set of characteristics that make it exceptionally well-positioned for the current macro environment: the world's lowest-cost offshore production base, six consecutive years of production growth with three more years of visibility, a 7%+ dividend yield, and zero downstream exposure in a regime of spiking crude prices. Against a backdrop of the most severe Middle East supply disruption in recorded history, CNOOC's geographically diversified, domestically anchored production base is not merely insulated from the crisis — it is a direct beneficiary.

The deeper investment thesis rests on China's unwavering commitment to energy security. With Beijing directing $468 billion into domestic E&P over five years, mandating new strategic reserve buildout, and treating offshore production as a matter of national security, CNOOC's regulatory and budgetary environment is the most supportive in the global oil industry. This state-strategic alignment — uncommon among listed companies — insulates CNOOC from the capital allocation volatility, activist shareholder pressure, and energy transition uncertainty that constrains Western majors.

The principal risk is the valuation discount itself: as long as U.S. investors cannot own CNOOC shares and China-related geopolitical risk commands an equity risk premium, the gap between intrinsic and market value may persist. But for investors in markets not subject to U.S. sanctions restrictions, this discount represents an attractive entry point into one of the world's best-positioned energy companies at a structurally pivotal moment in global hydrocarbon history.

Sources: CNOOC Limited 2025 Annual Results (March 2026), 2024 Annual Results, 2025 Interim Results, 2025 Strategy and Development Plan; CICC, DBS, Goldman Sachs analyst reports; South China Morning Post; Reuters; Al Jazeera; BNEF; BloombergNEF; China Daily; Enerdata; MarketScreener.

#cnooc #china #refining #refinery #explorationandproduction #alltimehigh #costefficiency #oilprice #crudeoil #naturalgas #sustainability #windpower #oilandgas

Communicator

Add Message