The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

The new podcast from ppPLUS. Join industry experts finding strategies for today's challenges.

Strategic Insight | ppPLUS Intelligence Series • Petrochemical & Chemical Industry | April 2026

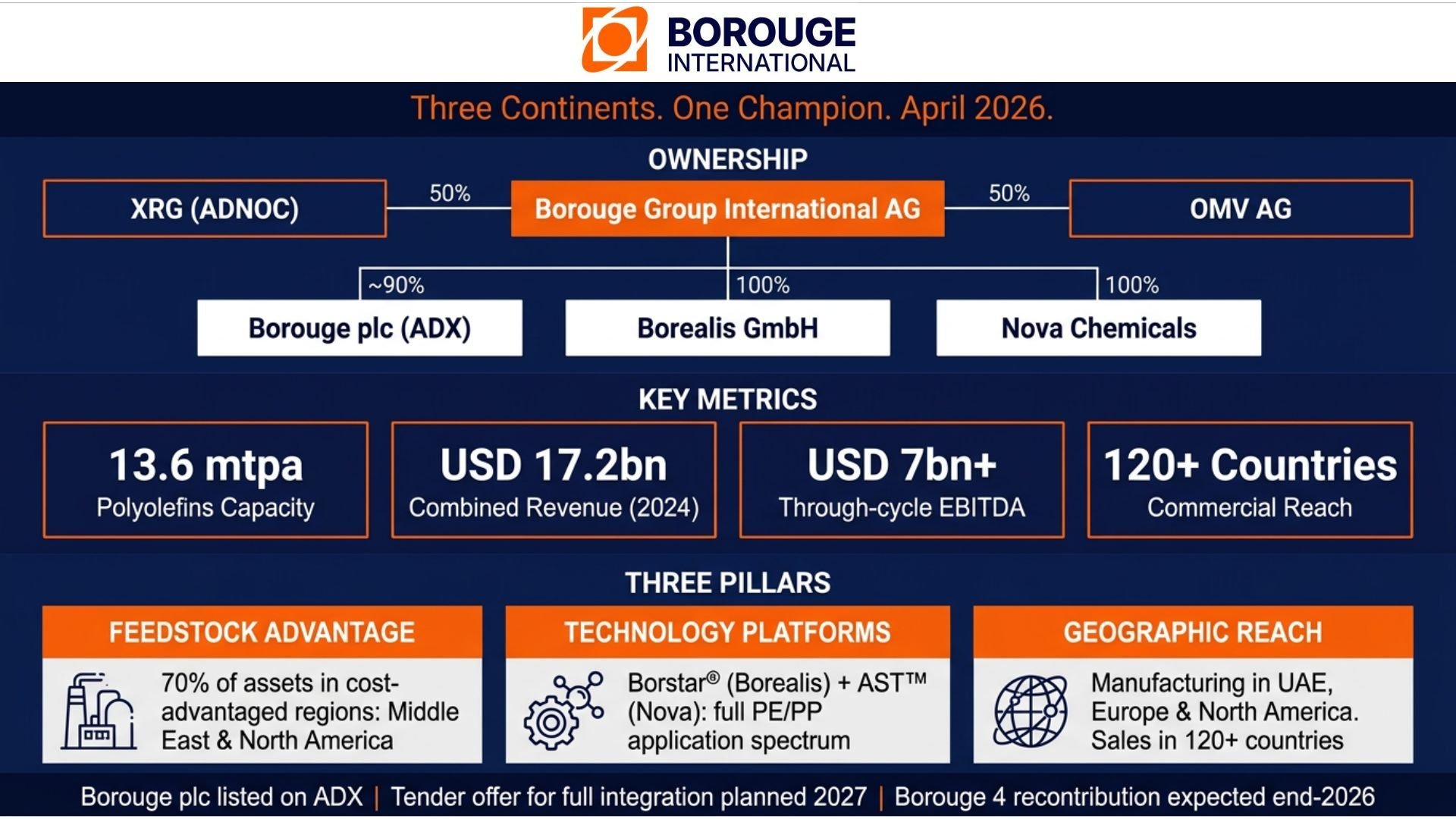

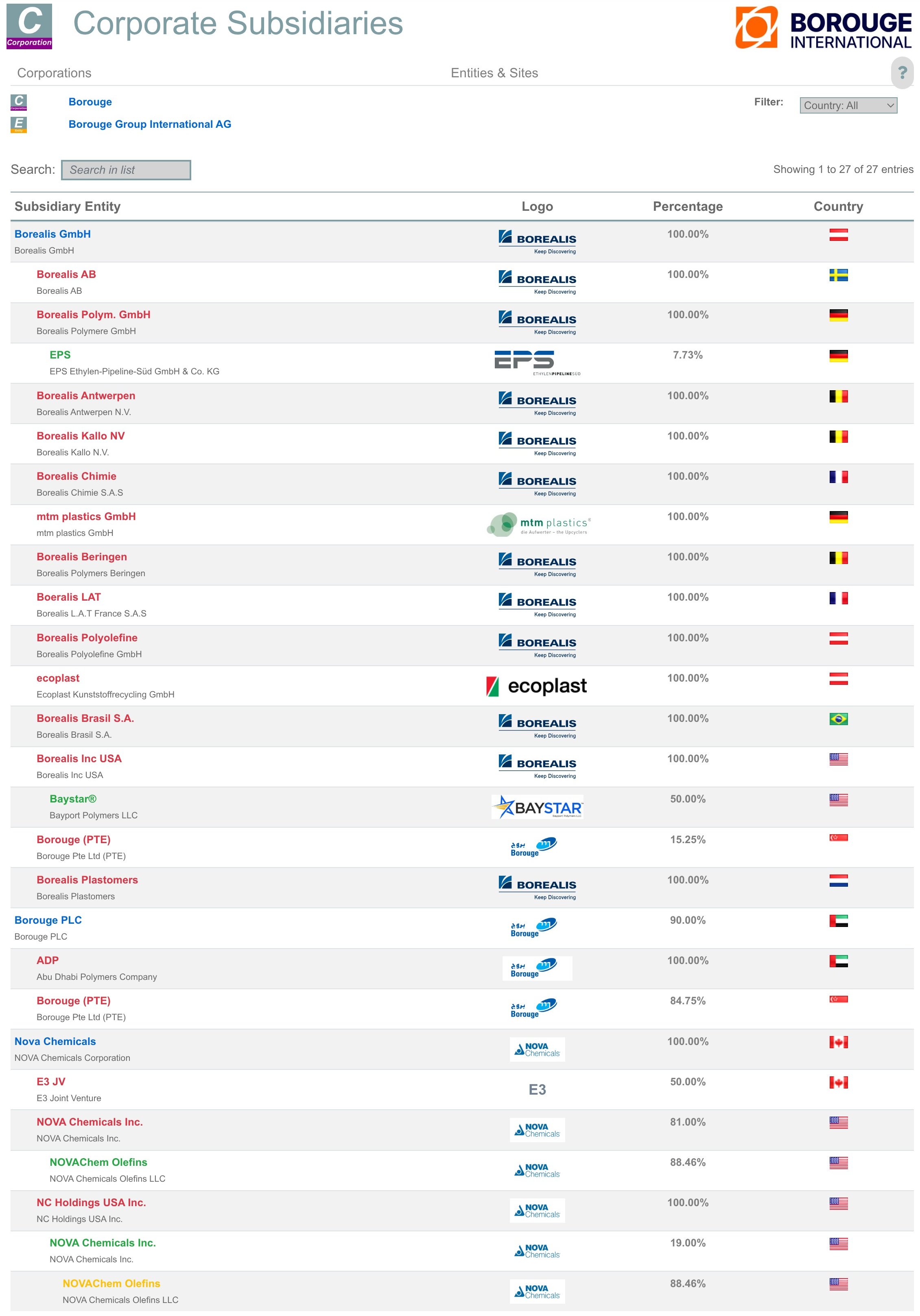

Corporate structure of the newly formed Borouge Group International GmbH as recorded on ppPLUS

Each of the three constituent entities brought a distinct but incomplete strategic profile. Borouge plc offered world-class feedstock cost advantage via ADNOC's Ruwais ethane supply, but was largely Middle East and Asia-focused. Borealis contributed technology leadership — its proprietary Borstar® polyolefin platform underpins some of the most advanced polyethylene (PE) and polypropylene (PP) grades globally — alongside a deep European industrial and customer footprint. Nova Chemicals added North American polyethylene scale, plugging the one geographic gap that had long limited both Borouge and Borealis from being considered a true global tier-1 player. Together, the combined entity commands 13.6 mtpa of capacity across three continents and revenues of USD 17.2 billion — credentials that place it firmly alongside LyondellBasell, Dow, and SABIC in the industry's top tier.

Borouge facility | Source: Borouge website

Critically, this is not merely a scale play — it is a cost structure transformation. Approximately 70% of production assets in the combined group are located in first-quartile, feedstock-advantaged regions: ~50% in the Middle East (Ruwais) and ~20% in North America (Nova's Alberta and Ontario assets, which benefit from cheap NGLs). This is a structural competitive advantage at a time when European crackers are under severe pressure from high energy costs and overcapacity in China. Once Borouge 4 is fully integrated into BGI by end-2026, the Middle East share of capacity will rise to approximately 47% of the group total.

Nova Corunna (St-Clair) during turnaround in 2022

Borouge International inherits what is arguably the most sophisticated proprietary polyolefin technology portfolio of any pure-play producer in the world. At its core sit two complementary and independently developed process platforms: Borealis' Borstar® — a gas-phase/slurry loop bimodal process covering both PE and PP, dominant in pipe, geomembrane, wire & cable, and infrastructure applications — and Nova's Advanced SCLAIRTECH™ (AST), a dual-reactor solution polymerization process that excels in high-performance film, flexible packaging, and specialty LLDPE grades. Complementing the process platforms, Nova's proprietary in-house catalyst program (including metallocene and post-metallocene systems) and its newly commercialized SYNDIGO™ recycled PE technology extend the group's reach into circular economy solutions. Together, these platforms cover virtually the entire polyethylene application spectrum, positioning Borouge International not merely as a commodity polymer producer, but as a specialty and advanced materials platform serving high-value segments including power cable insulation (XLPE), healthcare, energy infrastructure, sustainable packaging, and circular plastics.

Borstar plant at Borealis Burghausen facility in Germany | Source: Borealis web site

The 50/50 XRG–OMV ownership structure at BGI level is notable for its strategic symmetry: ADNOC/XRG brings feedstock security, sovereign balance-sheet support, and growth capital; OMV brings European market access, technology stewardship, and ESG credibility in a regulatory environment increasingly demanding circular economy credentials. The €1.6 billion cash equalization payment by OMV to achieve parity signals genuine long-term commitment rather than opportunistic positioning. That said, governance under a 50/50 structure historically introduces decision-making friction, and how BGI manages strategic divergences between its two principals — particularly on capital allocation between Middle East expansion versus European reinvestment — will be a key watch point.

Borouge International has declared a leadership position in circular solutions as a core strategic pillar, building on Borealis' established EverMinds™ circular economy program and Borouge's sustainability initiatives in the UAE. With regulatory pressure mounting across the EU (Extended Producer Responsibility, Single-Use Plastics Directive) and the Gulf (UAE Net Zero 2050), the group's scale gives it both the R&D budget and the production flexibility to develop recyclable, bio-based, and low-carbon polyolefin grades at commercial volumes — a capability smaller competitors simply cannot match.

Integration complexity: Three corporate cultures (Emirati, Austrian, Canadian), three legal systems, and three operational models must be unified without disrupting customer relationships or operational continuity

Borouge 4 recontribution: The planned recontribution of Borouge 4 into BGI by end-2026 must be executed cleanly, as the asset carries an estimated USD 7.5 billion price tag and will significantly reshape BGI's balance sheet

Tender offer execution (2027): Converting Borouge plc ADX free-float shareholders into BGI shares requires careful management of price discovery and investor acceptance in the UAE capital market

China competition: The structural overcapacity in Chinese polyolefins — with Chinese producers expanding aggressively on coal-to-olefins pathways — continues to compress global commodity margins, testing even feedstock-advantaged producers

This insight draws on the following sources: Borouge Group International Transaction Investor Presentation (March 2025); ADNOC and OMV press releases on the formation and completion of Borouge Group International AG (March–April 2026); Borealis Standalone Annual Report 2025; Borealis GmbH Investor Presentation 2025; Borouge 4 Re-contribution Overview (March 2025); S&P Global Ratings analysis of Borealis AG (March 2025); OMV and XRG transaction completion announcements (March 31, 2026); Borouge Investor Relations disclosures (ADX); and media coverage from ADNOC, Borealis, Zawya, Gulf News, and The National (2025–2026).

#adnoc #omv #borouge #borougeinternational #borealis #novachemicals #polyolefins #borstar #sclairtech

Communicator

Add Message