Mayday: The Global Jet Fuel Supply Chain in Free Fall

Grounded Virgin Australia aircraft parked at Brisbane Airport in Brisbane on April 7, 2020 due to Coronavirus Pandemic | Source: The Guardian • Photograph: Darren England/AAP

Market Insights | ppPLUS Intelligence Series • Geopolitics & Supply Chains | June 2026

The Crisis in Context

The warnings from IATA Director General Willie Walsh at the association's annual summit in Rio de Janeiro in June 2026 were stark and unusually direct: rising jet fuel prices driven by the war between the United States / Israel, and Iran are likely to push more airlines into bankruptcy and accelerate industry consolidation. Walsh did not mince words:

"Unfortunately, I think some airlines are going to find it very difficult to deal with these higher fuel prices"

and he expects some carriers to fail and their assets to be absorbed by larger competitors. These are not hypothetical warnings. They are the product of structural supply chain weaknesses that have been decades in the making, now exposed suddenly and violently by geopolitics.

To understand why the disruption is so acute, and why it cannot be quickly fixed, it is necessary to follow jet fuel from the wellhead to the wing.

How Jet Fuel Is Made — and Why Not Just Anywhere

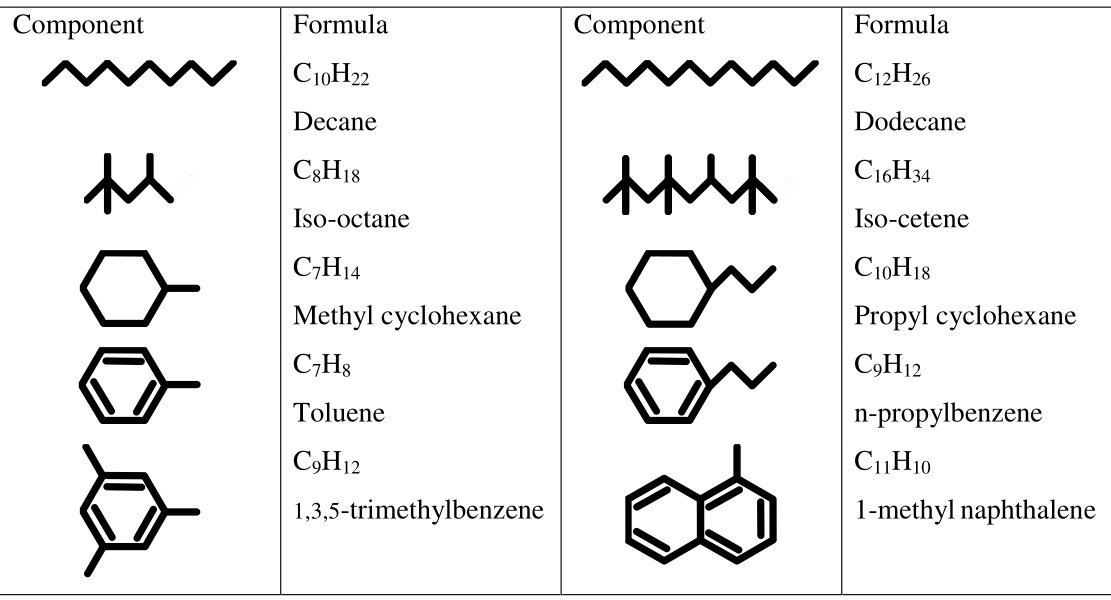

Jet fuel (Jet-A, or kerosene-type aviation turbine fuel) is produced by the fractional distillation of crude oil in the 150–250 °C boiling range, yielding what refiners call the "straight run kerosene" cut. According to the US Energy Information Administration, a typical 42-gallon barrel of crude oil processed at US refineries in 2023 yielded only 4.41 gallons of kerosene-type jet fuel, versus 19.57 gallons of motor gasoline and 12.47 gallons of distillate fuel oil. That narrow kerosene yield fraction — roughly 10% of a barrel — means jet fuel is structurally the most supply-constrained of the major transportation fuels. You cannot simply "turn up the dial" at a refinery to produce more of it without sacrificing other product yields and without the right crude feedstock.

Typical components of jet fuels | Source: M. Reza Kholghy / ResearchGate (Sep 2012)

Not all crude oils are equal in their jet yield. Heavier, high-paraffin crude oils from the Middle East — such as Arab Light, Kuwait Export Crude, and Iraqi Basrah Light — are particularly well-suited to maximising the kerosene cut after upgrading through hydrocracking. Modern complex refineries, especially those in the Persian Gulf, have been purpose-built and optimised over the past two decades to maximise middle-distillate yields, including jet fuel, from these feedstocks. Kuwait KIPIC's Al-Zour refinery, at 615,000 barrels per day (b/d) capacity with a Nelson Complexity Index of 7.1, and Saudi Arabia's SATORP refinery at 460,000 b/d with an NCI of 11.9, are archetypal examples of this design philosophy. These facilities were not built to serve domestic aviation — they were built to export jet fuel to Europe and Asia.

The Persian Gulf: Dual Role in Global Jet Supply

The Persian Gulf countries play not one but two pivotal roles in global jet fuel supply:

-

Direct export of refined jet fuel. Before the current conflict, refineries in the Gulf — primarily Kuwait, Saudi Arabia, and the UAE — produced and exported roughly 20% of the world's seaborne jet fuel, a share approximately double that of seaborne diesel. The majority of these exports flowed to Europe.

-

Feedstock supply to Asian mega-refineries. Between 40% and 60% of the crude oil processed by major Asian refining hubs in China, South Korea, India, and Thailand passed through the Strait of Hormuz. These Asian refineries then used that Gulf crude to produce jet fuel for both domestic consumption and export to third markets, including the US West Coast, Australia, and East Africa.

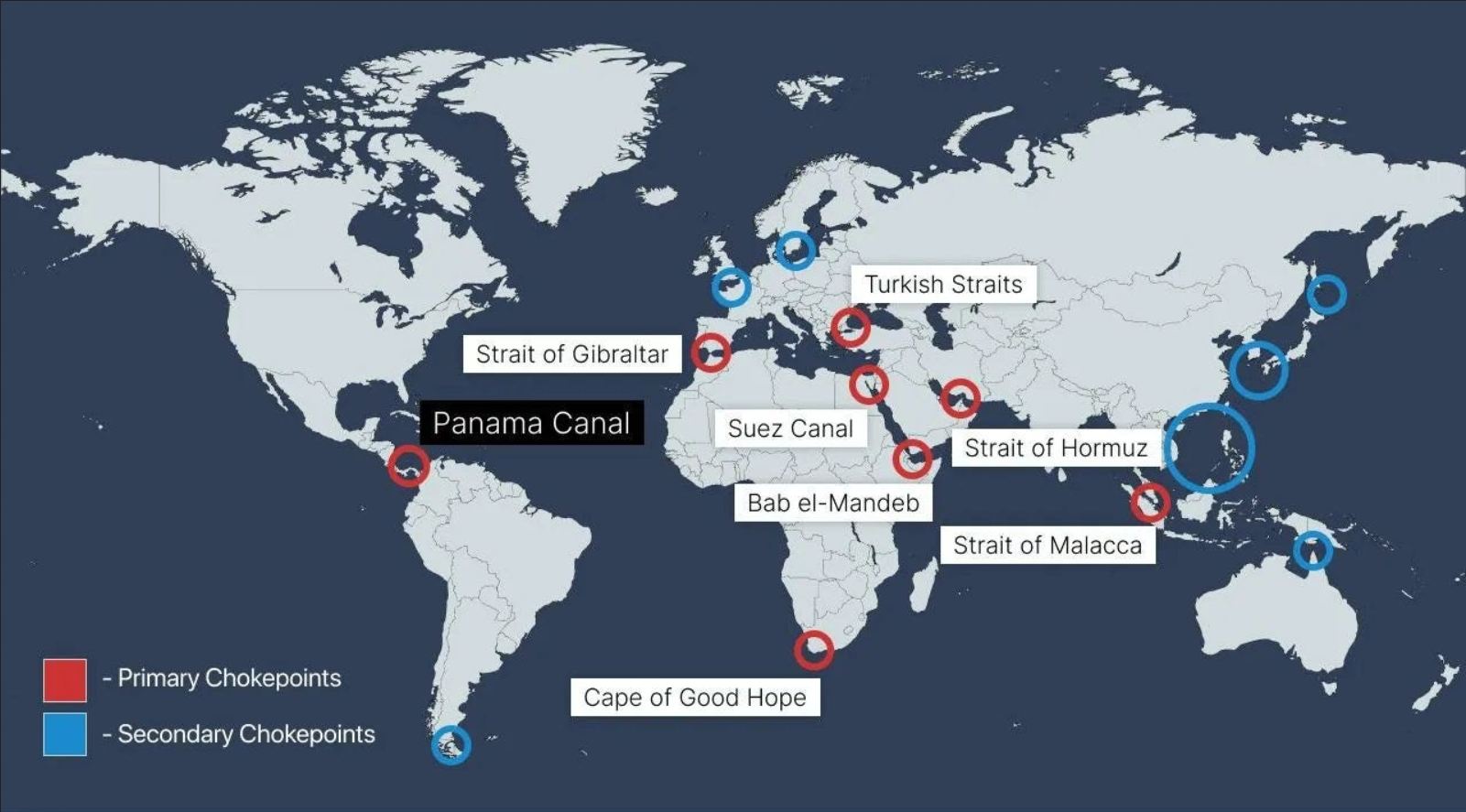

Global Maritime Choke Points | Source: Internet

The Strait of Hormuz — a chokepoint approximately 33 kilometres wide at its narrowest navigable point — is therefore the single most critical node in the global jet fuel supply chain. When Iran effectively closed the Strait following the escalation of the conflict in late February 2026, tanker traffic collapsed by 70–80%, according to IATA. The result was a simultaneous disruption to both direct Gulf jet fuel exports and to the crude feedstock supply of Asian export refineries — a double blow that no other single geographic chokepoint could replicate.

The Asian Refining Hub: Structurally Dependent on Gulf Crude

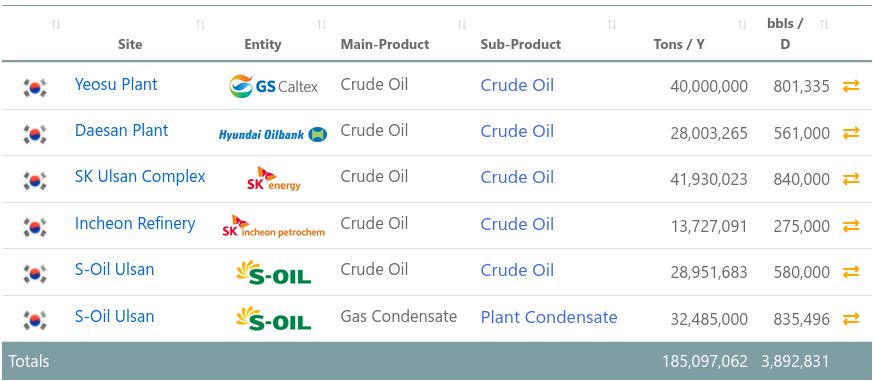

Asia is home to the world's greatest concentration of current and planned refining capacity. South Korea, in particular, has built one of the most export-oriented and complex refining systems in the world, with facilities such as SK Energy's Ulsan refinery and GS Caltex's Yeosu refinery operating among the highest Nelson Complexity Indexes globally. These are not primarily domestic-consumption refineries — they function as export hubs for middle distillates, including jet fuel, serving markets from California to East Africa.

South Korea alone accounted for over 82% of jet fuel imports to the US West Coast in 2025, totalling over 109,000 b/d. China and Japan supplied roughly 10,000 b/d and 6,000 b/d respectively. When the Strait of Hormuz shut down and Gulf crude stopped flowing to Korea, Korean refiners cut their run rates and prioritised domestic supply, halting exports. US West Coast jet fuel prices hit an all-time high in mid-April 2026 as South Korean supply dried up.

China, Thailand, and India responded similarly — restricting or banning jet fuel exports to preserve domestic inventories — cutting off the secondary markets that normally depend on Asian surplus.

The US Position: Better, But Not Immune

The United States is the world's largest crude oil producer, at approximately 13.2 million b/d, and operates one of the largest and most complex refining systems globally. On paper, this should provide insulation from Middle East disruption. In practice, the picture is more complicated.

Nearly 70% of US refining capacity was configured to run most efficiently on heavy, sour crude oil — the type predominantly imported from the Middle East and Latin America — rather than on the light sweet shale crude that now dominates domestic US production. This structural mismatch was not an accident. In the decades before the US shale boom, when global light sweet crude supply was declining, US refinery owners invested heavily in coking and hydrocracking units to process cheaper, heavier imported crude and maximise high-value product yields including jet fuel. Running those units on light domestic shale crude is technically possible but economically inefficient — it underutilises expensive secondary processing equipment and reduces overall margins.

As a result, even during the current crisis, US refineries have been able to increase jet fuel production by only 2–4%. The US Gulf Coast is better supplied than Europe, and the continental US imports very little jet fuel or crude directly from the Middle East. But the US West Coast is a structurally isolated sub-market. California in particular imports approximately 30% of its crude from the Middle East and relies on Asian refineries — primarily South Korean — for a large share of its refined jet fuel. Two California refinery closures in late 2025 — Phillips 66's Wilmington & Los Angeles refining complex, and Valero's Benicia refinery — have further reduced domestic West Coast refining capacity, with analysts estimating the closures could increase the region's jet fuel import dependency by up to 100,000 tonnes per month.

Source: airlines.org (Aug 13, 2021)

The Jones Act — which prohibits non-US-flagged vessels from carrying goods between US ports — makes it economically impractical to redirect Gulf Coast jet fuel surplus to the West Coast by sea, since the tanker freight cost from Houston to Los Angeles by Jones Act vessel is prohibitive relative to an import from South Korea. The April 2026 crisis forced Jones Act waivers and "airplane tankering" (ferrying fuel-laden aircraft between airports) as emergency measures, underlining the systemic vulnerability.

Europe: Most Exposed of All

Europe is the most acutely exposed major consuming region. According to IATA, between 25 and 30% of Europe's jet fuel demand originated from Persian Gulf refineries before the conflict. Kuwait has historically been Europe's single largest overseas supplier, with Saudi Arabia close behind. European refineries have seen significant capacity closures over the past decade as energy transition policies made investment uneconomical, reducing the continent's self-sufficiency in middle distillates.

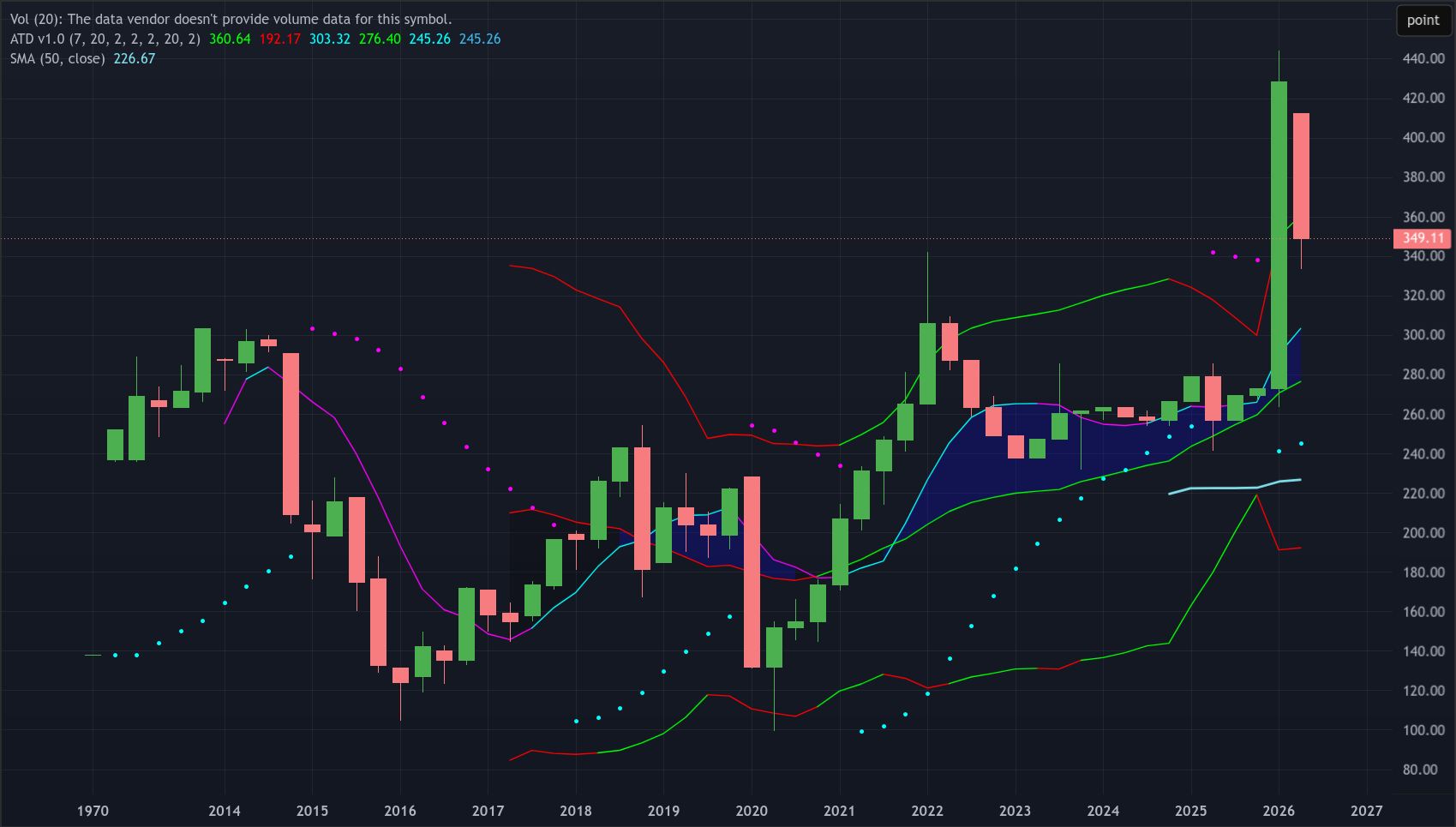

The IEA's Fatih Birol warned in April 2026 that Europe had "maybe six weeks of jet fuel remaining" if Gulf supply was not restored or substituted. Aviation fuel inventory in Europe typically represents just over one month of demand — a buffer that is structurally thin for a commodity that cannot be substituted. By May 1, 2026, European jet fuel prices had doubled year-on-year, reaching $187 per barrel. In April alone, global jet fuel exports fell 30% — from 19 million b/d to 13 million b/d — and weekly tanker loadings halved from 37.8 million barrels to 18.6 million barrels.

NIKKEI INC., TOKYO COMMODITY EXCHANGE, INC. (TOCOM) | Source: TradingView

Alternative suppliers — the US Gulf Coast, Nigeria, India — have been scrambling to fill the gap. However, the IEA itself estimated that even if all available alternative shipments were redirected to Europe, they would cover only slightly more than half of the lost Gulf volumes. Even if the Strait of Hormuz reopened immediately, transit times of up to two months mean the physical supply crunch in Europe cannot ease rapidly.

A Self-Inflicted Vulnerability

Long before the Strait of Hormuz closed, Western Europe had been systematically dismantling the refining infrastructure that had underpinned its jet fuel self-sufficiency for decades. The process accelerated sharply after February 2022, when Russia's invasion of Ukraine prompted the EU to implement, in close succession, a ban on seaborne Russian crude effective December 5, 2022, and a ban on Russian refined petroleum products effective February 5, 2023. These measures removed at a stroke what had been up to 27% of total EU crude imports and a significant share of direct middle-distillate imports, including diesel and jet fuel. The structural hole left by that withdrawal was never fully repaired.

European refineries had been configured over decades to run Russian Urals — a medium-sour crude that yields high proportions of distillates including kerosene — and reorienting them to alternative feedstocks such as West African crudes or North Sea light grades required blending workarounds, yield penalties, and in some cases, expensive secondary-unit upgrades that were simply not economically viable given the deteriorating outlook for fossil refining in Europe. Between 2020 and 2024, European refining capacity shrank by approximately 600,000 b/d, from 15.3 mb/d to 14.7 mb/d, while EU refinery runs in 2025 stood around 500,000 b/d below pre-COVID 2019 levels. From late 2024 to 2025 alone, four European refineries ceased crude processing, removing a further 400,000 b/d from the market.

| Refinery | Company | Country | Capacity |

|---|---|---|---|

| Grangemouth | Petroineos | Scotland, UK | 150,000 b/d |

| Wesseling (Rheinland) | Shell | Germany | 147,000 b/d |

| Horst / Scholven refining complex (partial) | BP Gelsenkirschen | Germany | ~85,000 b/d (one third of 257,000 b/d total) |

| Livorno (late 2024) | Eni | Italy | 84,000 b/d |

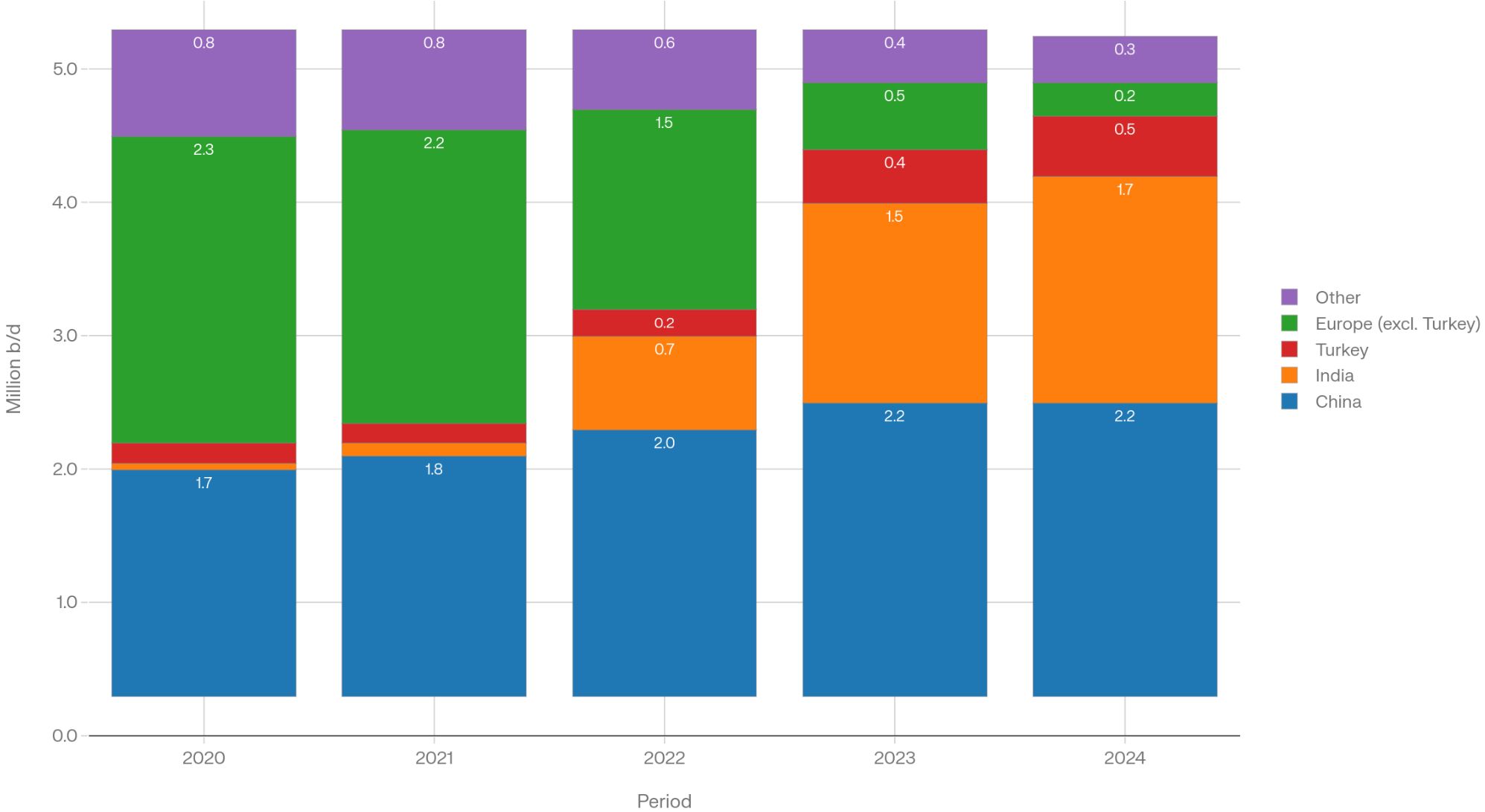

The gap was filled largely by replacing Russian barrels with Gulf product exports: between 2022 and 2025, Europe increased its imports from Gulf Cooperation Council (GCC) refineries by 230,000 b/d to 700,000 b/d, with diesel and jet fuel together accounting for nearly 70% of that total, Saudi Arabia and Kuwait covering approximately 80% of it. In 2025, Kuwait and Saudi Arabia collectively supplied 9.7 million metric tonnes of jet fuel to the EU and UK — 36% of the region's total consumption. Europe had thus traded one geopolitical dependency (Russia) for another (the Persian Gulf), without building the domestic buffer that could have bridged a sudden disruption in either direction.

The EU's 18th sanctions package, which introduced an anti-circumvention ban on products refined from Russian crude in third countries such as India and Turkey — effective January 2026 — cut off yet another informal relief valve that had been quietly supplying Russian-origin middle distillates through laundering refineries, particularly to the UK, which Global Witness had documented as sourcing up to one barrel in twenty of its jet fuel from Russian-crude-fed Indian refineries in 2023.

Sources: EIA, Reuters, KSE Institute, CREA

With product stocks in Europe already below the five-year average going into the Hormuz crisis, distillate crack spreads in Northwest Europe already elevated from the late-2025 Ukrainian drone campaign against Russian refining infrastructure, and Russian jet fuel exports formally banned by Moscow for a second consecutive cycle through November 2026, Europe entered the current supply shock in a structurally weakened position that is, to a considerable degree, the product of its own policy choices made with geopolitical and climate rationale, but without adequate preparation for the supply security consequences.

Why Refined Jet Fuel Cannot Be Easily Substituted

Unlike motor gasoline or diesel, jet fuel has no meaningful alternative that can be deployed at scale in the near term. Aviation turbine engines require a fuel with a precise combination of energy density, freeze point, viscosity, lubricity, and flashpoint. There is no "flex fuel" aviation engine. Airlines cannot switch to LNG, hydrogen, or electricity on existing aircraft. Even blending SAF above the current 50% certified limit requires re-certification.

This is the crux of the vulnerability that the IATA has been warning about for years and that the current crisis has made viscerally apparent. SAF total global production in 2025 reached only 1.9 million tonnes — less than 0.7% of total jet fuel consumption. LanzaJet's celebrated Freedom Pines plant, producing its first on-spec jet fuel from ethanol (ATJ) in late 2025, has a production capacity of just roughly 30,000 tonnes per year. The entire global SAF industry, across all pathways, represents a few weeks of European jet demand. At current build-out rates, even the most optimistic 2030 SAF projections — 17 million tonnes per annum — would still cover only 4–5% of total jet demand.

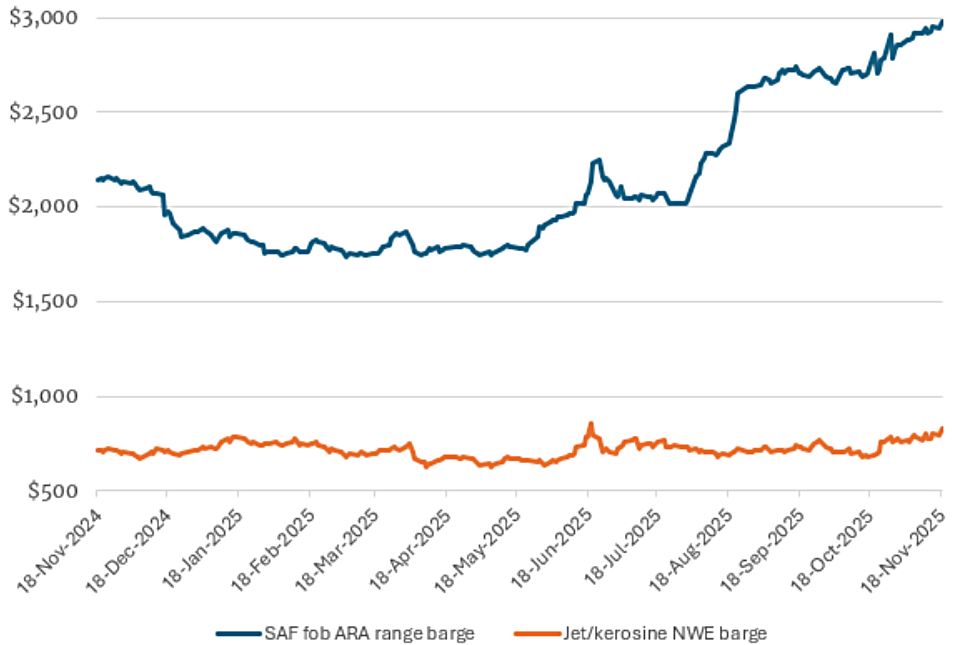

Compounding the volume problem is price. SAF currently costs between two and five times more than conventional fossil jet fuel, with most commercially available bio-SAF pathways — HEFA, ATJ — clustering at the lower end of that range, and electrofuels (e-SAF, Power-to-Liquid) at the extreme upper end, where production costs can reach ten times the fossil jet benchmark. In concrete market terms, industry analysis from early March 2026 showed California SAF pricing at approximately 8.85 USD/gallon against conventional jet at 3.59 USD/gallon — a ratio of roughly 2.5× even before the full force of the Hormuz disruption was felt. IATA's own modelling assumes an average SAF price of approximately 2,872 USD per tonne (374 USD per barrel) for 2026 supply volumes, a premium that — applied even to the sub-1% share SAF currently occupies in global jet demand — adds an estimated 4.3 billion USD to aggregate airline fuel costs. The World Economic Forum projects that SAF prices will remain two to three times higher than fossil jet fuel through at least 2030, absent transformative policy support or step-change reductions in green hydrogen costs.

Fossil jet vs. Bio-SAF (HEFA-SPK) Price Nov 2024→Nov 2025 • USD/tonne

Chart: Argus Media

This means that SAF cannot function as a demand-side buffer in a price crisis: it is structurally additive to cost pressure, not a relief valve. Airlines already absorbing a doubling of fossil jet prices cannot turn to SAF as a cheaper or even cost-equivalent substitute — the premium is permanent until scale, learning curves, and carbon pricing converge at a level the industry has not yet approached.

IATA's Risk Assessment: Well-Founded

Walsh's warnings about airline bankruptcies and consolidation are grounded in clear financial mechanics. Jet fuel typically represents 20–30% of an airline's operating costs in normal market conditions. At $187/barrel — double the year-ago level — fuel becomes the dominant cost line, and for airlines without fuel hedging programmes or with thin balance sheets, the margin compression is existential.

IATA's own research notes that sudden fuel price shocks are more destructive than elevated-but-stable prices, because revenues — ticket prices, cargo yields — adjust far more slowly than costs. Airlines that sold tickets months in advance at pre-shock fares are now fulfilling those bookings at post-shock fuel costs. Carriers that are financially weak, heavily exposed to leisure price-sensitive markets, or operating in regions where regulatory frameworks prevent rapid fare adjustment — particularly in Southeast Asia, South Asia, and parts of Africa — face acute near-term distress.

NASDAQ | Source: TradingView • JetBlue Airways is the most prominent current example —

a publicly traded US carrier now widely described as the airline closest to bankruptcy

in the developed world, with the fuel price crisis as the decisive factor.

The consolidation dynamic Walsh describes is also historically consistent: the oil shocks of 2008 and 2011 each triggered waves of airline failures and mergers, ultimately strengthening the balance sheets and network positions of surviving flag carriers and low-cost operators with fuel-efficient fleets.

The Structural Lesson

The current crisis is not simply the product of an unexpected war. It is the product of a global jet fuel supply chain that has been optimised over decades for cost efficiency rather than resilience, with:

- refining capacity increasingly concentrated in the Persian Gulf and Northeast Asia,

- consuming regions — especially Europe and the US West Coast — allowed to run down domestic refining capacity under energy transition pressure,

- strategic jet fuel reserves that amount to barely one month of demand in the most exposed markets,

- and no scalable fuel substitute that can be deployed in time to matter.

The IATA is right to flag airline bankruptcies as a near-term risk. But the deeper risk, as this crisis illustrates, is systemic: the global aviation network is operating with essentially zero slack in its primary fuel supply chain, and the geography of that supply chain is structured around a single chokepoint that a regional military confrontation can shut down within days.

Editorial note: The analysis and editorial judgements in this article are the authors' own. The factual record draws upon the following sources • International Air Transport Association (IATA) • Oxford Institute for Energy Studies (OIES) — Bassam Fattouh and Andreas Economou • OPIS / Hydrocarbon Processing • Energy Intelligence • BBC News • PBS NewsHour • CNBC • The World / PRI • American Petroleum Institute (API) • RBN Energy • S&P Global Commodity Insights • Jordan News • International Business Times (Singapore) • US Energy Information Administration (EIA) • American Fuel & Petrochemical Manufacturers (AFPM) • Fuel Stream Services • Reuters • Heartland Institute / Ronald Stein • Energy News Beat • Energy Security Freedom (Substack) / Ronald Stein • Global Witness, Energy and Clean Air Research Centre • Eurostat • European Commission • The Moscow Times • OilPrice.com • OPIS • Offshore Technology • Kuwait Petroleum / Economy Middle East • LanzaJet.

#jetfuel #jeta1 #kerosene #middledistillate #gasoline #refining #saf #sustainableaviationfuel #hefa #alcoholtojet #atj #distillatefueloil #refining